Have you ever wondered why two people can walk into the same bank, ask for the exact same loan amount, and walk out with completely different monthly payments? It feels a bit like a secret club where the entry fee is hidden behind a three-digit number. We’ve all heard that “credit is important,” but rarely do we see the actual cold, hard math of how a few points on your score can translate into thousands of dollars in or out of your pocket. It’s not just a grade; it’s the most powerful financial lever you own, and in 2026, lenders are looking at these numbers with more scrutiny than ever before.

When we talk about the relationship between Credit Score vs Interest Rate (Real Table), we are really talking about risk. To a bank, your credit score is a crystal ball. They use it to predict whether you’ll be a reliable partner or a financial headache. The higher your score, the less “danger” you represent, and the more the bank is willing to “discount” the cost of borrowing money. If you’ve been ignoring that little number on your banking app, it’s time to stop. We are going to break down the tiers, look at a real-world simulation, and show you exactly how much your reputation is worth in today’s market.

The Invisible Tiers of Lending

Lenders don’t just see a “good” or “bad” score; they work within specific brackets. While every bank has its own “secret sauce,” most of the industry follows a tiered structure. In 2026, the gap between these tiers has widened. A “Good” score used to get you the best rates, but now, lenders have introduced “Super Prime” categories for those at the very top.

If you are in the 780-850 range, you are the “Super Prime” darling. You get the red carpet treatment, the lowest APRs, and often, waived processing fees. As you drop into the 660-720 range, you’re still “Prime,” but you’ll notice the interest starts to creep up. Once you dip below 620, you enter the “Subprime” territory, where the rates don’t just increase—they explode. Understanding where you sit in this hierarchy is the first step to negotiating a better deal.

The Real Table: $35,000 Auto Loan Simulation

To make this practical, let’s look at a simulation for a $35,000 car loan with a 60-month (5-year) term. These numbers represent the average market rates we are seeing in April 2026 for borrowers across different credit tiers.

| Credit Tier | Score Range | Est. APR | Monthly Payment | Total Interest Paid |

| Super Prime | 781 – 850 | 4.8% | ~$658 | ~$4,480 |

| Prime | 721 – 780 | 6.2% | ~$680 | ~$5,800 |

| Near Prime | 661 – 720 | 8.5% | ~$718 | ~$8,080 |

| Subprime | 601 – 660 | 11.9% | ~$776 | ~$11,560 |

| Deep Subprime | 300 – 600 | 17.5% | ~$880 | ~$17,800 |

The Shocking Truth: Look at the difference between “Super Prime” and “Deep Subprime.” For the exact same car, the person with the lower score pays $13,320 more in interest. That is almost 40% of the car’s original price just in “interest tax.” When you see it laid out in a Credit Score vs Interest Rate (Real Table), the motivation to fix your credit becomes much more than just a suggestion—it becomes a financial emergency.

The “Cost of Waiting” vs. “Buying Now”

One of the most common questions I get is: “Should I buy the car now with my 640 score, or wait six months to get to 700?” This is where the opinion of a real expert comes in. If waiting six months means you can jump from “Subprime” to “Near Prime,” you could save over $3,500 in interest on that $35,000 loan.

Is six months of your time worth $3,500? For most people, that’s a resounding yes. However, if your current car is breaking down and costing you $500 a month in repairs, the math changes. You have to weigh the “interest penalty” against the “repair penalty.” Sometimes, the best move is to take the high-interest loan now but make sure it has no prepayment penalty, so you can refinance the moment your score improves.

Is it Worth It?

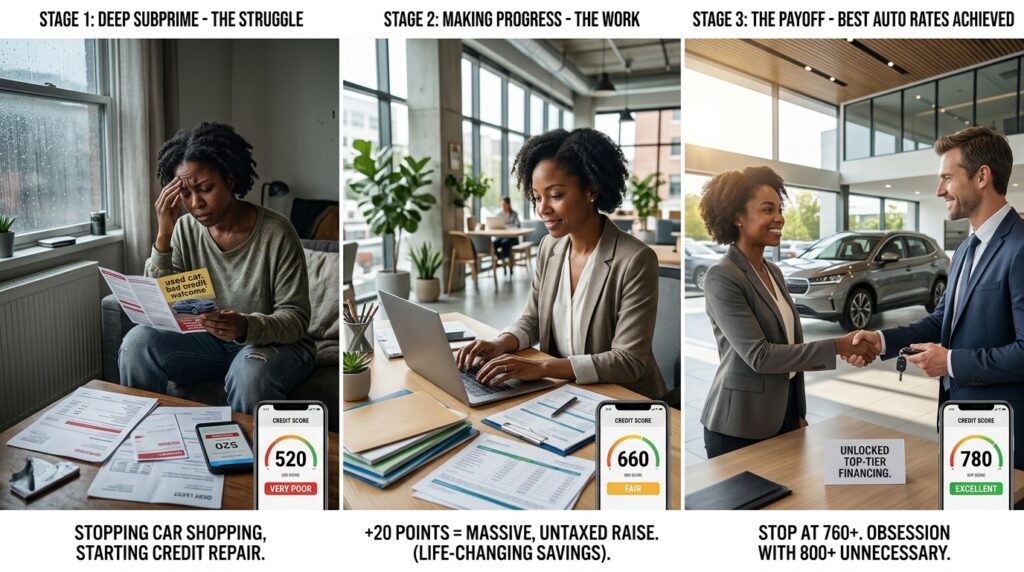

Is it truly worth the obsession with hitting a 800+ score? There is a point of diminishing returns. Once you cross the 760 or 780 threshold, you’ve already unlocked the “Best Auto Loan Rates in 2026.” Moving from a 800 to a 850 won’t usually get you a lower rate; it just gives you “bragging rights.”

The real “worth it” zone is moving from the 500s into the high 600s. That is where the most life-changing savings happen. If you are currently in the “Deep Subprime” category, your primary job shouldn’t be car shopping—it should be credit repairing. Every 20 points you gain is like giving yourself a massive raise that isn’t taxed. It is the most efficient way to increase your net worth without working a single extra hour at your job.

What to Consider Before Choosing a Lender

Before you let a dealership run your credit (which can actually lower your score slightly), consider these three factors that determine how your Credit Score vs Interest Rate (Real Table) experience will go:

1. The “Hard Inquiry” Cluster

When you apply for a loan, it creates a “hard pull” on your credit. In 2026, credit models are smart; if you have five car loan inquiries in a 14-day window, they count it as one single event because they know you’re just shopping. But if you spread those inquiries over two months, your score will take a hit. Shop fast and shop focused.

2. Debt-to-Income (DTI) Matters Too

A 800 credit score is great, but if 60% of your income is already going toward other debts, a bank might still give you a higher interest rate or deny you altogether. Your credit score shows your reliability, but your DTI shows your capacity. You need both to be in good shape to get the rates at the top of the table.

3. The Type of Vehicle

Believe it or not, the car itself affects the rate. In 2026, many lenders offer “Green Discounts” for EVs or Hybrids. You might find that a 700 score gets you a 5% rate on an electric car but a 6.5% rate on a heavy-duty gas truck. The bank views the EV as a more “future-proof” asset with better resale value, lowering their risk.

Important Tips

-

Check for Errors First: About 20% of credit reports have mistakes. Before you apply for a loan, use a free service to ensure there aren’t “ghost debts” dragging your score down. Fixing a single error can jump your score 40 points in a month.

-

The 30% Utilization Rule: If your credit cards are maxed out, your score will suffocate. Try to pay them down so you’re using less than 30% of your limit at least 30 days before you apply for a big loan. This is the fastest way to “artificially” boost your score for the table.

-

Join a Credit Union: Big national banks are often rigid with their Credit Score vs Interest Rate (Real Table) tiers. Local credit unions are more likely to look at the “human” side and might give a “Near Prime” borrower a “Prime” rate if they have a long-standing relationship.

-

Don’t Close Old Accounts: The age of your credit history matters. Even if you don’t use that old card from college, keep it open. It proves you’ve been managing credit for a long time, which lenders love to see.

The Psychological Weight of a Score

We treat credit like a cold math problem, but it’s deeply psychological. Having a low score feels like a weight on your shoulders—it limits where you can live, what you can drive, and how you plan for the future.

On the flip side, having a high score provides a sense of financial “gravity.” Things just cost less for you. You have more leverage in negotiations. When you walk into a dealership knowing you are a “Super Prime” borrower, the power dynamic shifts. You aren’t asking for a favor; you are offering them the privilege of your business. That confidence, backed by a solid number, is the ultimate goal of credit management.

Conclusion: Take Control of Your Number

As we’ve seen in the Credit Score vs Interest Rate (Real Table), the difference between an average score and a great score isn’t just a few dollars—it’s a massive fortune over the course of your life. Whether you are buying a car today or planning for a house in three years, your credit score is the foundation of your financial house.

Don’t settle for “Deep Subprime” rates if you can help it. Use the tools available to you, pay down your balances, and watch the doors to lower interest rates swing open. In the world of 2026, information is power, and knowing exactly how your score dictates your expenses is the first step toward true financial freedom.

Take a look at your score today, compare it to our table, and decide: are you going to pay the “interest tax,” or are you going to keep that money for yourself? The choice, and the work, is yours. Happy saving!