The prospect of driving a brand-new car off the lot today and not worrying about a single payment for ninety days sounds like a dream. In the automotive industry, these are known as Deferred Payment Car Loans, often marketed with catchy slogans like “No Payments for 3 Months” or “Drive Now, Pay Later.”

In the financial climate of 2026, these offers have become increasingly popular as manufacturers look for ways to lower the barrier to entry for new buyers. However, while they provide immediate breathing room for your bank account, they are not a “get out of jail free” card. There is a complex mechanical process happening behind the scenes with your interest and principal.

To be a smart buyer, you need to understand that “deferred” does not mean “deleted.” In this guide, we will break down exactly how these loans work, the hidden costs you need to watch out for, and how to use them strategically without hurting your long-term financial health.

What Exactly Is a Deferred Payment Car Loan?

At its core, a deferred payment car loan is a standard auto loan where the lender agrees to push back the start date of your first monthly installment. Typically, a car payment is due 30 days after you sign the contract. With a deferral, that date might be moved to 60, 90, or even 120 days in the future.

This is a common tactic used during year-end sales events or economic downturns to stimulate buying. The dealership gets to move inventory, and the buyer gets to enjoy their new vehicle immediately without an instant hit to their monthly cash flow.

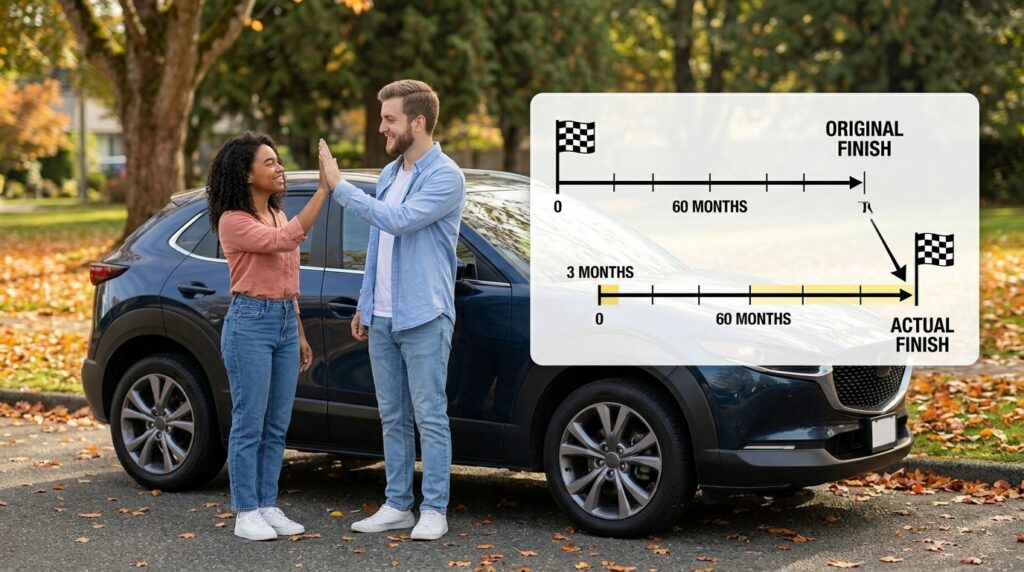

However, it is vital to remember that the loan term itself doesn’t change—only the start date. If you have a 60-month loan and you defer for 3 months, you still have 60 payments to make; you’ve just pushed the “finish line” three months further down the road.

The “Silent” Math: How Interest Accrues

The most important thing to understand about deferred payments is how interest is calculated. In the vast majority of car loans, interest is simple interest, and it is calculated daily based on the current balance of the loan.

When you defer your payments, the interest does not stop. It continues to accumulate from the day you drive the car home. This is often referred to as “accrued interest.”

The “First Payment” Shock

Because interest has been building for 90 days before you make your first payment, that first check you write will go almost entirely toward interest. Very little, if any, will go toward the actual principal (the price of the car). This means you aren’t actually making progress on paying off the vehicle during those first few months; you are simply treading water.

The Long-Term Cost

Because the interest starts accruing on the full purchase price immediately, a deferred loan will always cost more over the life of the loan than a standard loan. Even a 90-day deferral can add several hundred dollars to the total cost of the car because you are paying interest on interest.

Why Lenders Offer These Deals

You might wonder why a bank would want to wait for their money. The answer is simple: it makes the “yes” easier.

Lenders know that the biggest hurdle to a car sale is the “double-whammy” of a down payment followed immediately by a monthly bill. By removing that second hurdle, they can close more deals. Furthermore, because you end up paying slightly more in total interest, the deferral is actually a more profitable product for the lender in the long run.

In 2026, many manufacturers use their “captive” finance arms (like Toyota Financial or Ford Credit) to offer these deals. They view the slight loss in immediate cash flow as a worthwhile trade-off for moving high-value inventory off the lot.

The Benefits of Deferring Your Payments

Despite the extra interest costs, there are legitimate, “smart” reasons to choose a deferred payment option.

1. Managing a Transition

If you are starting a new job and won’t receive your first full paycheck for six weeks, a 90-day deferral can be a lifesaver. It allows you to secure reliable transportation to get to that new job without the stress of an immediate bill.

2. Consolidating Debt

Some buyers use the “payment-free” window to pay off a high-interest credit card or another smaller debt. By redirecting the money they would have spent on a car payment toward a 24% interest credit card, they can actually come out ahead financially, even after accounting for the car loan’s accrued interest.

3. Recovering from the Down Payment

If you pushed your budget to make a substantial down payment (which we always recommend), a deferral gives you a few months to replenish your “emergency fund” or savings account before the regular monthly bills begin.

The Risks: When “Pay Later” Becomes a Problem

While the benefits are clear, the risks of deferred payments can be subtle and long-lasting.

1. Faster Negative Equity

As we’ve discussed in other guides, cars depreciate the moment they leave the lot. If you aren’t making payments for the first three months, your loan balance stays at the maximum while the car’s value drops.

This puts you in a state of negative equity (being “underwater”) much faster. If you total the car in those first three months, you will owe the bank the full price of the car plus three months of interest, while the insurance company will only pay the depreciated market value.

2. The Lifestyle Inflation Trap

The biggest psychological risk is that you get used to “not having a car payment.” You might adjust your lifestyle and spending habits during those three months, only to find that when the bills finally start arriving, your budget is too tight to handle them.

3. Higher Total Debt

If you are already on a tight budget, the extra interest added to the back end of the loan might push your total debt-to-income ratio higher than you’d like. Over a 72-month loan, that “free” 90 days could cost you $500 to $800 in extra interest—money that could have gone toward maintenance or insurance.

How to Handle a Deferral Like a Pro

If you decide to take a deferred payment offer, there are ways to mitigate the downsides.

Pay the Interest Only

Some smart buyers will make “interest-only” payments during the deferral period. This prevents the interest from ballooning and ensures that when your regular payments start, they immediately begin attacking the principal balance of the car.

Make a Larger Down Payment

To counteract the negative equity risk, put more money down upfront. If you put 20% down, the fact that you aren’t making payments for 90 days won’t matter as much because you’ll still owe less than the car is worth.

Set the Money Aside

Even if you don’t have to pay the bank, “pay yourself.” Put your projected car payment into a separate savings account every month during the deferral. By the time your first bill arrives, you will have a three-month “cushion” sitting in your bank account, ready for any emergencies.

Deferred vs. Skipped Payments: What’s the Difference?

It is important to distinguish between a Deferred Payment Car Loan (set up at the start of the purchase) and a Payment Deferral Request (asking for help because you can’t pay).

-

At Purchase: This is an incentive. It is structured into the contract and is usually a sign of a “deal” being made.

-

During the Loan: If you lose your job and ask the bank to skip a month, this is a hardship request. While banks often allow this once or twice, it usually comes with fees and can sometimes negatively impact your credit if not handled correctly.

Reading the Fine Print in 2026

Before you sign a “Pay Later” contract, you must ask the finance manager three specific questions:

-

Is interest accruing during the deferral period? (The answer is almost always yes, but you want to hear them say it).

-

Does this deferral change my APR? Some lenders offer 0% APR only if you start payments immediately, but will charge 2.9% if you choose the deferral.

-

Is there a “deferral fee”? Some non-manufacturer lenders charge a flat fee to set up a deferred schedule.

Is a Deferred Payment Car Loan Right for You?

Ultimately, a deferred payment car loan is a tool. Like any tool, it can be used to build or to break.

If you use the 90-day window to stabilize your finances, pay off higher-interest debt, or build an emergency fund, it is a brilliant move. If you use it to buy a car you can’t actually afford, hoping that “future you” will somehow have more money in three months, it is a recipe for disaster.

In 2026, the smartest car buyers are the ones who look at the Total Cost of Ownership, not just the date of the first bill. If the total interest cost of the deferral fits within your long-term plan, go for it. If not, stick to the standard schedule and start building equity in your new ride from day one.

Summary Table: Standard vs. Deferred Loans

Final Thoughts

The allure of “driving now and paying later” is strong, but a smart buyer always keeps a calculator in their pocket. A deferred payment car loan provides flexibility, but flexibility always comes at a price.

Understand the math, respect the interest accrual, and make sure that when those payments eventually start, you are ready to hit the ground running. Your car should be a source of freedom, and knowing exactly how your loan works is the best way to keep it that way.