In the high-pressure environment of a car dealership in 2026, the moment you transition from the showroom floor to the finance office is where the real “game” begins. You’ve found the car, but now you have to pay for it. For many buyers—especially those with a few bumps in their credit history—the phrase “In-House Financing” starts to sound like music to their ears.

In-house financing, often associated with “Buy Here, Pay Here” (BHPH) dealerships, means the dealer isn’t just selling you the car; they are acting as the bank. There is no middleman, no third-party lender, and often, a much lower barrier to entry. But in 2026, where digital tracking and high-interest rates are the norm, is this a path you can trust?

To be a smart buyer, you need to understand the mechanics of in-house loans. While they offer a lifeline to mobility, they also come with a unique set of risks that can either rebuild your financial life or bury it. Let’s break down the reality of dealership loans.

How In-House Financing Works in 2026

Traditional financing involves a dealership sending your information to a bank or credit union. The bank decides if you are a “safe bet” and sets the terms. With in-house financing, the dealer uses their own capital to fund the loan.

They aren’t necessarily looking for a high FICO score. Instead, they focus on your proof of income and stability. In the current market, dealers are increasingly using digital verification tools to see your real-time cash flow. If you can prove you have a steady paycheck and a permanent address, you’re likely to be approved on the spot.

This “one-stop-shop” convenience is the primary draw. You pick the car, sign the paperwork, and drive off the lot within a couple of hours, regardless of what happened to your credit three years ago.

The Trust Factor: Can You Believe the Dealer?

The question of “trust” in dealership loans isn’t about whether the loan is legal—it usually is—but whether the terms are transparent. Because the dealer holds all the cards, they have the power to set interest rates and vehicle prices that are significantly higher than the market average.

The Profit Double-Dip

When you finance in-house, the dealer makes money twice: once on the sale of the car and again on the interest of the loan. In 2026, interest rates for in-house financing can frequently hit 18% to 25%.

A smart buyer must ask: “Am I paying a premium for the car AND a premium for the money?” Often, a car that would sell for $10,000 elsewhere is priced at $13,000 at a BHPH lot. When you add high interest on top of an inflated price, you are starting your journey in a deep hole of negative equity.

The Pros: When Dealership Loans Are the Right Move

Despite the higher costs, there are specific scenarios where in-house financing is a mechanical necessity for a buyer’s life.

1. Absolute Approval Flexibility

If you are a recent immigrant, a college student with zero credit, or someone recovering from a major financial setback, a traditional bank will likely decline your application. In-house lenders are much more “human” in their evaluation. They care that you have a job today, which can be the difference between having a way to work or being unemployed.

2. Speed and Simplicity

There is no waiting for a bank’s underwriting department to open on Monday morning. Everything is handled in one room. For someone who needs a car immediately to keep their life moving, this speed is a massive value proposition.

The Cons: The Hidden Costs of Convenience

The trade-off for “easy approval” is often a loss of financial flexibility and a higher risk of losing the vehicle.

1. The Starter-Interrupt and GPS Norm

In 2026, almost all in-house financing vehicles are equipped with GPS trackers and starter-interrupt devices. If you are even a few days late on a payment, the dealer can remotely disable your car. While this helps the dealer mitigate risk, it adds a layer of stress to the buyer. If you have an emergency and miss a payment by 48 hours, you might wake up to a car that won’t start.

2. High Frequency of Repossession

Because the standards for approval are lower, the default rates are higher. Many in-house dealers are “repossession-heavy.” Their business model relies on you making payments for a year, defaulting, and then them taking the car back to sell it to the next person. To trust an in-house loan, you must be 100% certain that your income is stable enough to never miss a payment.

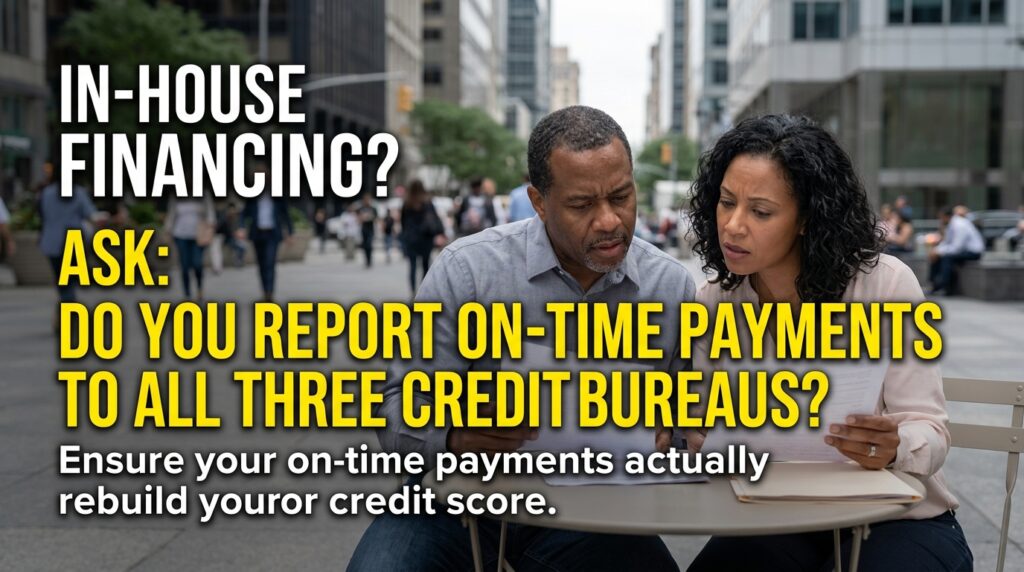

The “Credit Building” Trap: A Crucial Distinction

One of the biggest reasons people choose in-house financing is the hope of rebuilding their credit. However, this is where many buyers are misled.

Not all in-house dealers report to credit bureaus. If you make every payment on time for three years but the dealer doesn’t report it to Equifax, Experian, or TransUnion, your credit score will not move a single point. You will have paid 24% interest for years and still have “bad credit” at the end of it.

Before you sign, you must ask one specific question: “Do you report my on-time payments to all three major credit bureaus?” If the answer is “no” or “only if you default,” you are being denied the primary benefit of subprime financing.

Red Flags to Watch For in the Finance Office

If you decide to move forward with a dealership loan, keep your guard up for these common 2026 “tactics”:

-

“Yo-Yo” Financing: If a dealer lets you drive off the lot but tells you the “final” terms aren’t set, walk away. They may call you a week later saying the interest rate went up or they need more money down.

-

Mandatory Add-Ons: Be wary of “required” service contracts, GAP insurance at triple the market price, or window etching. These are often rolled into the loan, meaning you’re paying 20% interest on a $500 window sticker.

-

Refusing a PPI: If a dealer won’t let you take the car to an independent mechanic for a Pre-Purchase Inspection (PPI), they are likely hiding a mechanical issue. Remember: just because they are financing you doesn’t mean the car is in good condition.

Smart Strategies: How to Use In-House Financing Safely

If you need an in-house loan to get your life back on track, you can still play the game to your advantage.

Use it as a Short-Term Bridge

Never view an in-house loan as a 72-month commitment. View it as a 12-to-18-month bridge. Make every payment on time, ensure the dealer is reporting to credit bureaus, and the moment your score improves, refinance with a credit union or a traditional bank at a much lower rate.

Negotiate the “Out-the-Door” Price First

Dealers will try to focus you on the “weekly payment.” Ignore the payment and focus on the price of the car. If the car is worth $10,000, don’t pay $15,000 for it just because the financing is “easy.” The lower the purchase price, the less interest you’ll pay over time.

Verify the GPS Disclosure

Ask where the GPS and interrupt devices are installed and what the grace period is before they disable the car. A reputable in-house lender will be transparent about their security measures and won’t hide them in the fine print.

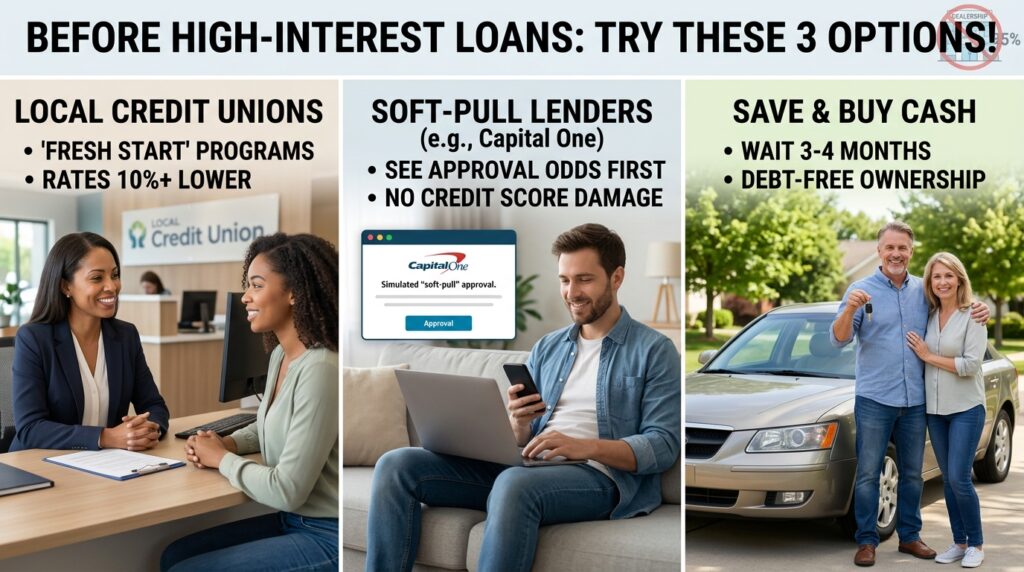

Better Alternatives (Check These First!)

Before committing to a high-interest dealership loan, exhaust these three options:

-

Local Credit Unions: They often have “Fresh Start” programs designed for people in your exact situation, with rates that are 10% lower than a BHPH lot.

-

Capital One or Carvana: These “soft-pull” lenders allow you to see your approval odds and rates without hurting your credit score. They are often more competitive than in-house options.

-

The “Save and Buy Cash” Route: If you can wait three to four months, the money you would have spent on a down payment and three months of high-interest installments could often buy a reliable, older vehicle outright.

Final Verdict: Should You Trust Dealership Loans?

Trust is a strong word. You should verify dealership loans rather than trust them. In-house financing is a powerful tool for those who have been shut out of the traditional financial system, but it is a tool with sharp edges.

If the dealer is manufacturer-approved, reports to the credit bureaus, and provides a clear history report for the car, an in-house loan can be a legitimate stepping stone. However, if the dealer is vague about reporting, inflates the car’s price by 50%, and uses high-pressure tactics, they are not a partner in your financial recovery—they are a predator.

In 2026, the smart buyer doesn’t just look for a “yes”; they look for a “yes” that leads to a better future. Do your homework, ask the hard questions about reporting, and always have an exit strategy to move toward cheaper credit as soon as possible.