Think back to the day you signed for your current car. You were likely caught up in the excitement of the test drive, the smell of the interior, and the urgent need to get the paperwork over with so you could finally hit the road. In that whirlwind, many of us settle for the first interest rate the dealership offers, often leaving hundreds—if not thousands—of dollars on the table. But here is the good news: just because you signed that contract a year or two ago doesn’t mean you’re stuck with it until the wheels fall off.

Car refinancing is one of the most underutilized tools in personal finance, especially as we navigate the economic shifts of 2026. It is essentially a “do-over” for your auto loan. By swapping your existing high-interest debt for a new loan with better terms, you can change your monthly budget overnight. Whether your credit score has improved, market rates have dipped, or you simply realized you got a raw deal at the dealership, understanding the “Refinancing Your Car: How Much Can You Save?” math is the first step toward reclaiming your hard-earned cash.

What Exactly is Auto Refinancing?

At its core, refinancing is simpler than it sounds. You aren’t actually “changing” your current loan; you are taking out a brand-new loan from a different lender to pay off the old one. The new lender sends a check to your old bank, the old lien is cleared, and you start making payments to the new guys under a different set of rules.

Why would a bank want to do this? Because they want your business. In 2026, the competition among credit unions and online lenders is fierce. They are willing to offer lower rates to “steal” a reliable borrower from a big national bank. From your perspective, nothing about the car changes—you still park it in the same spot—but the financial “weight” it carries becomes much lighter.

The 2026 “Why Now?” Factor

Timing is everything. In the current market, we are seeing a stabilization of interest rates after a period of volatility. If you took out a loan in early 2024 or 2025 when rates were peaking, there is a very high probability that you are overpaying by today’s standards.

Additionally, if you’ve been diligent about paying your bills on time over the last twelve months, your credit score has likely climbed. In the world of auto lending, the difference between a 640 score and a 720 score is massive. Refinancing allows you to “capture” the value of your improved financial reputation and turn it into a lower monthly payment.

Real-World Savings Simulation: The $30,000 Reset

Let’s look at a practical example of how the math shakes out. Imagine you bought a high-quality used truck 18 months ago.

The Original Loan:

-

Remaining Balance: $25,000

-

Current Interest Rate: 9.5%

-

Remaining Term: 48 Months

-

Monthly Payment: ~$628

The Refinanced Loan:

-

New Interest Rate: 5.5%

-

New Term: 48 Months (keeping the same timeline)

-

Monthly Payment: ~$581

-

Monthly Savings: $47

-

Total Interest Saved: ~$2,250

While $47 a month might not sound like a life-changing sum, look at that total interest figure. That is over $2,200 that stays in your pocket instead of going to the bank’s profit margin. That covers a set of new tires, several years of oil changes, or a nice boost to your holiday fund. And this is a conservative estimate—many people who move from “subprime” dealership rates to “prime” credit union rates save double that amount.

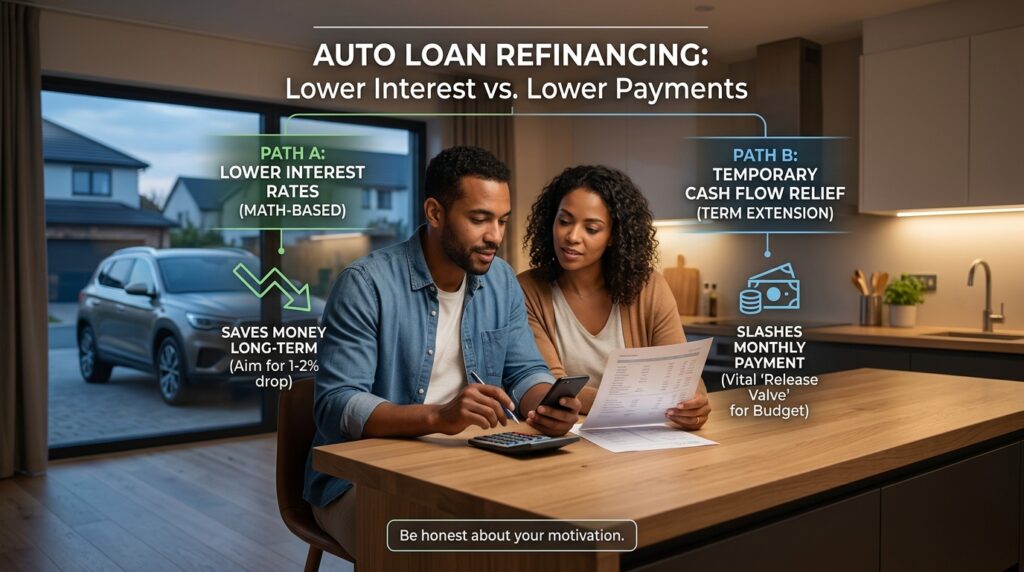

Is Refinancing Your Car Worth It?

This is the question that stops most people from acting. They worry the paperwork will be a nightmare or that the savings won’t justify the effort. From a purely mathematical standpoint, if you can drop your interest rate by at least 1% to 2%, it is almost always worth the effort.

However, it’s not just about the interest rate. Refinancing is also worth it if you are facing a temporary cash flow crisis. By extending your loan term (say, from 24 months remaining to 48 months), you can slash your monthly payment significantly. While this means you’ll pay more in interest over the long haul, it can be a vital “release valve” for your monthly budget during tough times. Just be honest with yourself about why you’re doing it.

Key Scenarios Where Refinancing Wins

There are four specific situations where you should be hunting for a refinance quote immediately:

1. Your Credit Has “Healed”

If you bought your car while you were still recovering from a bankruptcy, a divorce, or a period of unemployment, you likely got hit with a “risk premium” on your interest. If you’ve spent the last year rebuilding your score, you are no longer that “risky” borrower. The bank doesn’t know that unless you tell them by applying for a new loan.

2. You Finished the “Dealer Wait” Period

Many dealership loans include a “markup” where the dealer gets a kickback for signing you at a higher rate. Usually, you can refinance these loans after just 60 to 90 days. If you felt pressured into a high rate just to get the car home, wait three months and then jump ship to a credit union.

3. Market Rates Have Dropped

Macroeconomics matters. If the central bank has lowered rates since you bought your car, every lender in the country is now offering cheaper money. Don’t leave your loan in 2024 if it’s already 2026.

4. You Need to Remove a Co-signer

Life changes. Maybe you bought the car with an ex-partner or a parent, and you now want the title and the debt solely in your name. Refinancing is the cleanest way to “buy out” their responsibility and gain total financial independence over the asset.

Critical Factors to Consider Before Switching

Before you jump into a new contract, you need to check for “deal breakers.” Not every car is eligible for a refinance, and not every deal is a good one.

-

Vehicle Age and Mileage: Most lenders have a cutoff. If your car is more than 10 years old or has over 100,000 miles, it becomes much harder to find a competitive refinance rate. The car is the “collateral,” and banks are hesitant to lend against an asset that might not last the length of the loan.

-

The “Upside Down” Problem: If you owe $20,000 on a car that is only worth $15,000, you have “negative equity.” Most lenders will only finance up to 110% or 120% of the car’s value. If you’re too far underwater, you might need to bring cash to the table to close the gap before you can refinance.

-

Prepayment Penalties: Check your current contract. Some “predatory” loans include a fee if you pay them off early. If that fee is $500 but you’re only saving $400 in interest, the math obviously doesn’t work.

Expert Dicas: How to Get the Best Deal

-

Don’t Forget the Fees: Some states charge a small fee to transfer a title or re-register the lien. It’s usually between $15 and $75, but you should factor that into your “break-even” calculation.

-

Shop Around in a Short Window: When you apply for loans, it creates a “hard inquiry” on your credit. However, if you do all your shopping within a 14-day window, credit scoring models usually group them together as a single inquiry, protecting your score.

-

Check Your Local Credit Union: I cannot stress this enough. Big national banks often don’t care about a $15,000 auto refinance. Local credit unions love them. They often have the lowest rates and the most human-centered customer service.

-

Watch Out for “Loan Packing”: Just like at the dealership, some refinance companies will try to sell you extended warranties or life insurance during the process. Usually, these are overpriced. Just take the low interest rate and skip the extras.

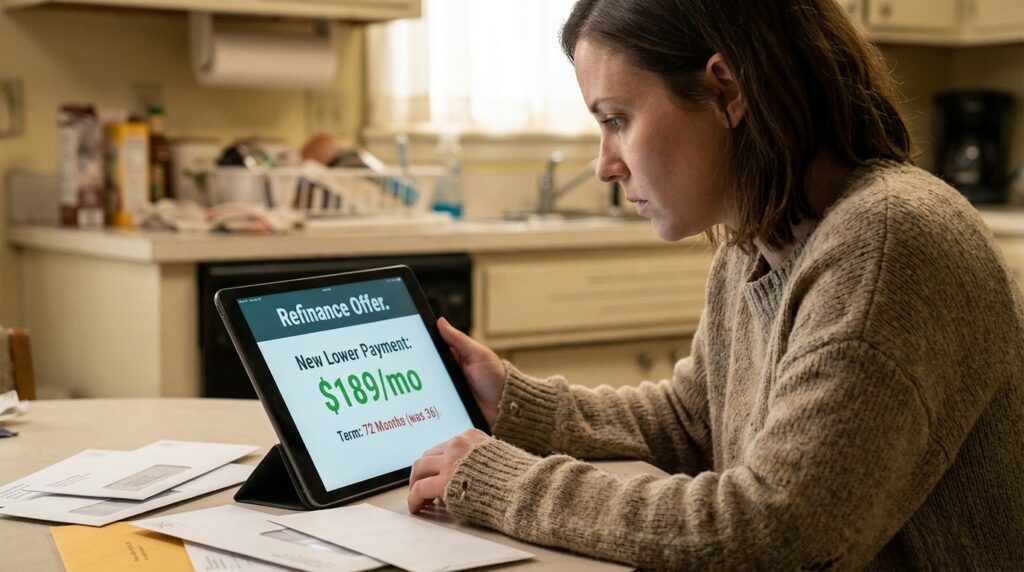

The “Term Extension” Trap

One thing to be very careful of is the temptation to lower your payment by stretching the loan out too far. If you have 3 years left on your loan and you refinance into a new 5-year loan, your monthly payment will be tiny, but you will pay much more in interest over time.

The “pro move” is to refinance for a lower rate but keep the same remaining time (or even shorter). This way, you save on interest and monthly cash flow without extending your debt into the next decade.

Conclusion: Take the 15-Minute Challenge

At the end of the day, Refinancing Your Car: How Much Can You Save? is a question only you can answer by taking action. It takes about 15 minutes to gather your current loan statement and run the numbers through an online calculator. Those 15 minutes could be the most profitable quarter-hour of your year.

Don’t stay loyal to a bank that is overcharging you. In 2026, the power is in the hands of the borrower who is willing to shop around. If you can save $50 a month, that is a subscription paid for, a few extra dinners out, or a faster path to being completely debt-free.

Take a look at your current APR today. If it’s in the high single digits or double digits, there is almost certainly a better deal waiting for you. Grab your documents, compare the rates, and start putting that interest money back where it belongs—in your own bank account. Safe driving and happy saving!