The automotive world has shifted gears faster than most of us anticipated. If you walked onto a car lot just a few years ago, the financing process felt like a predictable, albeit stressful, dance between the dealer and a few big banks. But today, in April 2026, the landscape is unrecognizable. We have fintech giants offering instant “tap-to-pay” financing, credit unions utilizing green-energy incentives, and a market that finally rewards the prepared buyer more than the lucky one. Whether you are eye-balling a high-tech EV or a reliable used truck, finding the right partner to fund that purchase is the difference between a smart investment and a decade of financial regret.

When we look at the Best Auto Loan Lenders in 2026 (Full List), we aren’t just looking at who has the lowest interest rate today. We are looking at the “total package”—the digital experience, the flexibility of the terms, and how they handle the “small stuff” like title transfers and gap insurance. Navigating this sea of lenders requires a bit of an insider’s perspective. It’s about knowing which bank likes your specific credit profile and which one is currently hungry for new business. Let’s break down the top contenders and the strategies that will save you the most money in this current economic climate.

The Landscape of Auto Financing Today

In 2026, the market is split into three main camps: the Digital Disruptors, the Traditional Titans, and the Community Champions. The Digital Disruptors are the apps on your phone that can approve a $50,000 loan in the time it takes you to order a latte. They focus on speed and transparency. The Traditional Titans are the big national banks that offer stability and massive loyalty rewards if you already have a mortgage or credit card with them.

The Community Champions, mostly local credit unions, have made a massive comeback this year. They are often the ones offering the most aggressive “Green Rates” for electric vehicles and more personalized service for those whose credit scores aren’t exactly “Super Prime.” Understanding which camp you belong in is half the battle. If you value speed, you go digital; if you value the lowest possible APR and don’t mind a bit of paperwork, you go local.

Best Auto Loan Lenders in 2026: Our Top Picks

To keep this list practical, we’ve categorized these lenders by what they do best. Remember, rates change weekly, so always treat these as a simulation of what the market is offering for a borrower with “Good” to “Excellent” credit (700+ score).

1. LightStream: Best for Excellent Credit

LightStream remains the heavyweight champion for people with high credit scores. Why? Because they offer unsecured auto loans. This means they deposit the cash directly into your bank account, and you go to the dealership as a “cash buyer.”

You don’t have to deal with the bank’s lien on the car title immediately, giving you massive leverage during price negotiations. In 2026, their “Rate Beat” program is still active—if you find a lower rate elsewhere, they’ll often beat it by a small percentage just to keep your business.

2. PenFed Credit Union: Best for Low Rates

You don’t have to be in the military to join Pentagon Federal Credit Union anymore, and that is a huge win for car buyers. In 2026, PenFed consistently sits at the top of the Best Auto Loan Lenders in 2026 (Full List) because of their sheer volume.

They offer incredibly competitive rates on both new and used vehicles. Their “Car Buying Service” is also a standout feature; if you use their portal to find the car, they’ll often shave another 0.5% off your APR. It’s a seamless way to combine the shopping and financing phases.

3. Capital One: Best Digital Experience

Capital One has perfected the “Auto Navigator” tool. This allows you to browse local dealership inventory and see your actual monthly payment on every car—including taxes and fees—before you even leave your couch.

It is a “soft pull” on your credit, meaning it won’t hurt your score to see what you qualify for. For the buyer who hates the mystery of the dealership finance office, Capital One offers the most “human” and transparent digital journey on the market today.

4. Consumers Credit Union: Best for New Vehicles

If you are looking for the absolute basement-level interest rates on a brand-new 2026 or 2027 model, this is usually where you find them. They are aggressive lenders who specialize in new vehicle acquisitions. While their membership requirements involve a small fee to a partner association, the savings on a 60-month loan often total thousands of dollars, making that small entry fee irrelevant.

Is it worth it?

Is it worth the extra time to shop for a lender, or should you just use the one the dealer recommends? In 2026, I would argue that shopping around is always worth it. The average “dealer markup” on an interest rate is about 1.5%. On a $40,000 loan, that extra 1.5% costs you roughly $1,600 over five years.

Even if you end up using the dealer’s financing because they have a manufacturer-subsidized rate (like 1.9% or 0%), having a pre-approval from one of the lenders on our list gives you a “floor.” It ensures the dealer can’t overcharge you because you already have a better deal in your pocket. The 20 minutes you spend applying online is essentially “earning” you hundreds of dollars an hour in future savings.

What to Consider Before You Choose

Before you commit to a lender, you need to look at more than just the percentage sign. Here are the three pillars of a “good” loan in today’s market:

1. The Pre-Approval Period

Some lenders only lock in your rate for 30 days. In 2026, with supply chain issues still occasionally affecting specific car trims, you might need 60 or even 90 days to find the right vehicle. Ensure your lender’s “lock-in” period matches your shopping timeline so your rate doesn’t expire while the car is in transit.

2. Gap Insurance and Protection

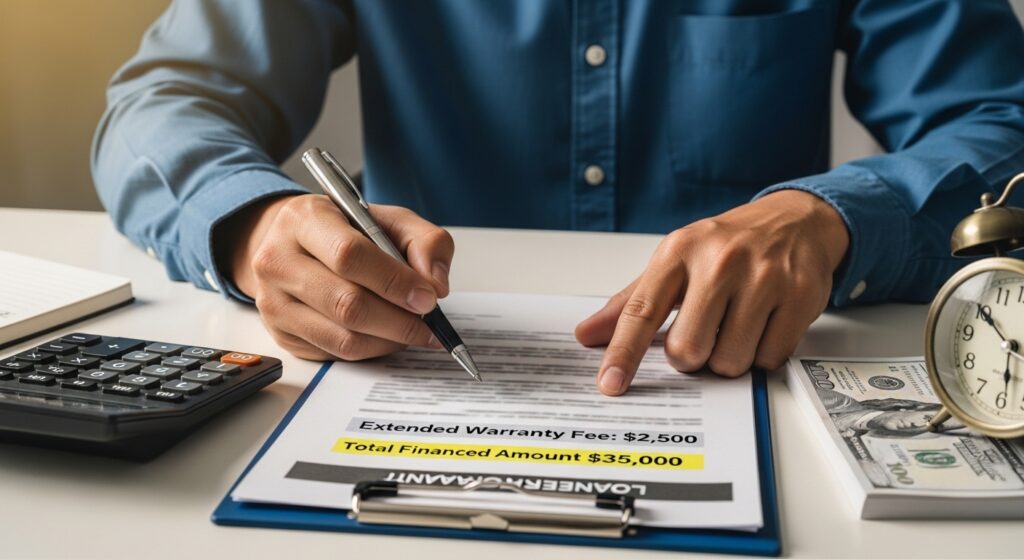

Does the lender offer Gap insurance? If you are putting less than 20% down, you are at risk of being “underwater” if the car is totaled. Dealerships often charge $800 to $1,200 for Gap insurance, but many of the Best Auto Loan Lenders in 2026 (Full List) offer it for a flat fee of $300 to $500. This is a massive hidden saving.

3. Payment Flexibility

Life happens. In 2026, the best lenders offer “Skip-a-Payment” features or easy online tools to change your payment date. If you get paid bi-weekly, finding a lender that allows bi-weekly automated drafting can save you a significant amount of interest over the life of the loan without you even feeling the difference in your budget.

Important Tips

-

The Credit Union Edge: Always check a local credit union before a national bank. Because they are member-owned, they don’t have to answer to shareholders, which often results in 1% to 2% lower rates for their members.

-

Auto-Pay Discounts: Almost every lender on the Best Auto Loan Lenders in 2026 (Full List) offers a 0.25% or 0.50% discount if you set up automatic payments. It’s “free” money—take it.

-

Refinance if You Must: If you had to take a bad deal at the dealership because you were in a rush, don’t sweat it. You can usually refinance a car loan within 30 to 60 days. Don’t feel “married” to a high-interest rate.

-

Watch the “New vs. Used” Line: In 2026, some lenders consider a “used” car to be anything with more than 5,000 miles, while others look at the model year. If you are buying a 2025 model with low mileage, check if you can still qualify for the lower “New Car” rates.

The Psychological Power of Choice

There is an underrated psychological benefit to walking into a dealership with a pre-approval letter. You stop being a “borrower” and you start being a “buyer.” When the salesperson asks, “What monthly payment are you looking for?” you can honestly answer, “I’m not looking for a payment; I’m looking at the out-the-door price, because my financing is already handled.”

This shift in the conversation is what prevents “loan packing”—the practice where dealers add extra warranties and fees into a monthly payment that “looks” affordable but is actually overpriced. By choosing your lender beforehand, you take the emotional pressure out of the finance office and keep it where it belongs: on the numbers.

Conclusion: Making the Final Call

Choosing the right partner from the Best Auto Loan Lenders in 2026 (Full List) isn’t just about the math; it’s about your peace of mind. If you are looking for the absolute lowest rate, look toward PenFed or a local credit union. If you want the most convenient, “see-everything” experience, Capital One or Carvana’s internal financing are hard to beat.

At the end of the day, the “best” lender is the one that fits your specific credit profile and provides the terms that let you sleep at night. Don’t let the excitement of a new car blind you to the reality of the contract. Take twenty minutes today to get a pre-approval. It is the single most effective way to ensure that your new car remains a source of joy, rather than a source of financial stress. You’ve done the research on the car—now do the research on the money. You’ll thank yourself every time you make that monthly payment. Safe driving!