The landscape of the driveway has changed quite a bit over the last few years, hasn’t it? Not long ago, we were dealing with empty dealership lots and prices that felt like a bad joke. Now, as we navigate through 2026, the inventory is back, but the financial side of the equation has become a whole different beast. If you’re looking to upgrade your ride, you’ve probably noticed that the “Best Auto Loan Rates in 2026 (Full Comparison)” isn’t just a list of numbers—it’s a moving target influenced by your credit score, the type of engine under the hood, and even where you choose to bank.

Shopping for a car loan today feels a bit like being a detective. You see a low rate advertised on a billboard, but by the time you sit in the finance office, that number has climbed three percentage points because of “market adjustments” or specific trim requirements. It’s frustrating, and frankly, it’s enough to make anyone want to just keep their old clunker for another decade. But don’t throw in the towel just yet. We’ve crunched the latest data to show you exactly where the deals are hiding and how you can snag a rate that won’t leave your wallet gasping for air.

The Current State of Interest: 2026 Reality Check

In 2026, we are seeing a fascinating “split” in the market. On one hand, traditional internal combustion engine (ICE) vehicles are seeing steady, if slightly higher, rates as lenders factor in long-term resale volatility. On the other hand, specialized “Green Loans” for electric vehicles (EVs) and high-efficiency hybrids are being heavily subsidized by both the government and manufacturers.

If you have a credit score north of 740, you’re still in the driver’s seat. However, for the average buyer, the days of “easy money” are gone. Lenders are looking closer at debt-to-income ratios than they have in years. This means that preparation is your best friend. You wouldn’t show up to a marathon without shoes, so don’t show up to a dealership without knowing your own financial stats first.

Breaking Down the Tiers: Who Offers the Best Rates?

When we look at the Best Auto Loan Rates in 2026 (Full Comparison), we have to categorize lenders into three main buckets. Each has its pros and cons, and where you fit depends entirely on your patience and your paperwork.

1. Credit Unions: The Local Heroes

Credit unions remain the hidden gem of the automotive world. Because they are member-owned and not-for-profit, they often pass the savings directly to you. In 2026, we’ve seen credit unions offering rates as much as 1.5% lower than national banks. They are especially great for used car loans, where big banks tend to hike the interest significantly.

2. Captive Lenders (Manufacturer Financing)

These are the big names—Ford Credit, Toyota Financial, GM Financial. They have one goal: to sell cars. If a specific model isn’t moving off the lot, they will offer “subvented” rates. We are talking 0.9% or even 0% APR on 36-month terms for specific 2026 models. The catch? You usually need “Super Prime” credit, and you might have to give up a cash rebate to get the low rate.

3. Online Lenders and Fintechs

This is the fastest-growing sector in 2026. Companies that live entirely on your smartphone can often give you an “instant” pre-approval. While their rates are competitive, they are often very strict about the car’s age and mileage. They are perfect for the “no-haggle” buyer who wants to walk into a dealership with a virtual check in hand.

Comparison Simulation: New vs. Used vs. EV

To make this practical, let’s look at a simulation for a $40,000 loan over a 60-month term across different categories based on 2026 average data.

| Vehicle Type | Average APR (Excellent Credit) | Monthly Payment | Total Interest Paid |

| New ICE Vehicle | 5.2% | $759 | $5,540 |

| Used Car (3 Years Old) | 7.8% | $807 | $8,420 |

| New EV (Green Loan) | 3.5% | $728 | $3,680 |

Looking at these numbers, the “Best Auto Loan Rates in 2026 (Full Comparison)” clearly favors the EV/Hybrid segment. Over five years, choosing the high-efficiency route could save you nearly $4,700 in interest compared to a used car loan. That’s a significant amount of cash that covers a lot of charging or gas.

Navigating the “Green Loan” Wave

If you’ve been on the fence about going electric, 2026 might be the year the math finally forces your hand. Many banks have introduced “Climate Positive” lending programs. These aren’t just marketing gimmicks; they are lower-interest products designed to meet corporate sustainability goals.

Beyond just the lower APR, these loans often come with perks like waived loan-origination fees or discounted insurance partnerships. If you’re looking for the absolute lowest total cost of ownership, starting your search specifically with “Green Auto Loans” is the smartest move you can make this year.

Making a Decision: What’s Actually Worth It?

Is it worth it to chase the lowest rate possible, or should you focus on other factors? In my experience, a low rate is great, but it shouldn’t be your only metric.

If you find a 0% APR deal but the car itself is marked up $5,000 over MSRP, you aren’t actually saving money—you’re just paying the interest upfront to the dealer instead of over time to the bank. Conversely, if you have to take a slightly higher rate (say 6% instead of 5%) to get a car that has a legendary reputation for reliability and low depreciation, that extra 1% is a price worth paying for peace of mind.

The most “worth it” deal is the one where the loan term matches your ownership plan. If you plan to keep the car for three years, don’t take a six-year loan just to get a lower monthly payment. You’ll end up “upside down” (owing more than the car is worth) and stuck in a debt cycle that is hard to escape.

Critical Factors to Weigh Before Signing

Before you commit to a specific lender, keep these 2026-specific considerations in mind:

-

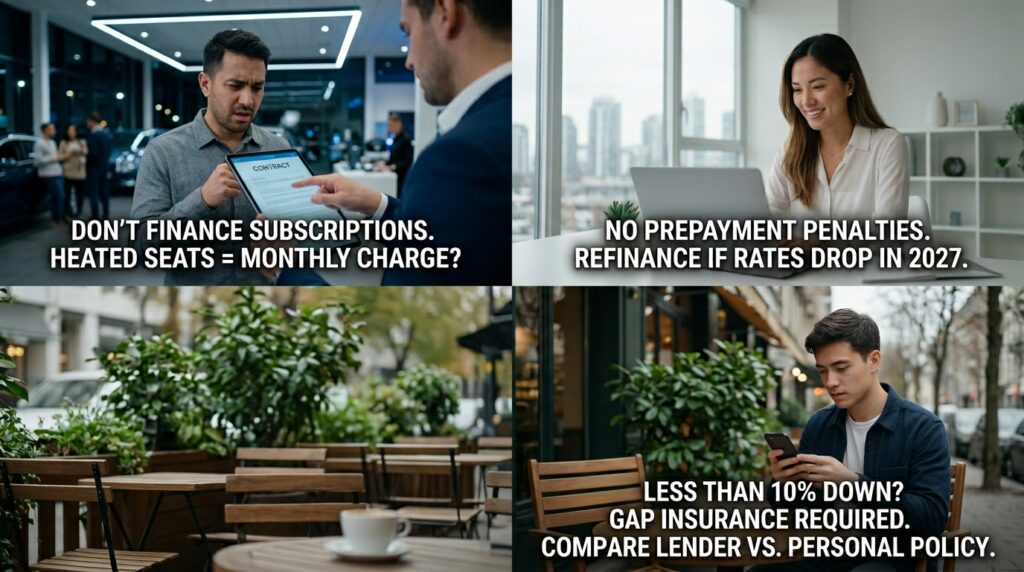

The “Add-on” Inflation: Dealerships are increasingly trying to wrap “Digital Subscriptions” and “Subscription-based heated seats” into the loan amount. Be very careful here. Financing a $20-a-month software feature over 60 months at 6% interest is a terrible financial move.

-

Refinance Flexibility: Ensure your loan has no prepayment penalties. The 2026 market is volatile; if rates drop in 2027, you want to be able to refinance that 7% loan down to a 4% without the bank hitting you with a “break-up” fee.

-

Gap Insurance Requirements: If you are putting less than 10% down, most lenders in 2026 will require Gap Insurance. Compare the lender’s price for this against your personal auto insurance provider; usually, your insurance company is much cheaper.

Pro-Tips for the 2026 Car Buyer

-

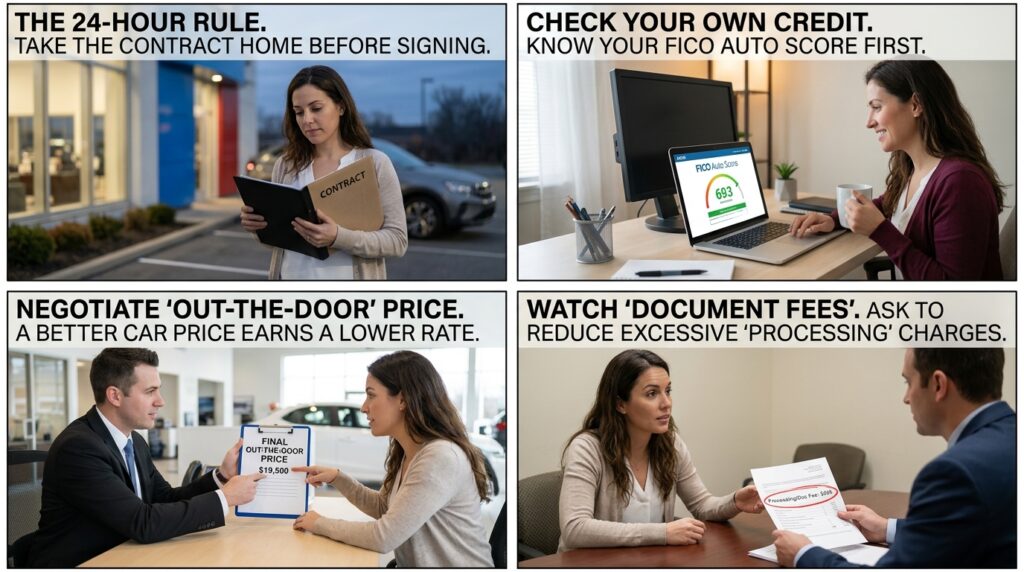

The 24-Hour Rule: Never sign the loan paperwork the same day you test drive. The “new car high” is a real thing, and it impairs your ability to do basic math. Take the contract home, look at the total cost of interest, and sleep on it.

-

Check Your Own Credit First: Don’t let the dealer tell you what your score is. Use a free tool to see your FICO Auto Score (which is different from your regular credit score). Knowing your number prevents them from “bumping” your rate for extra profit.

-

Negotiate the “Out-the-Door” Price: Lenders care about the “Loan-to-Value” ratio. If you negotiate a great price on the car, you’re more likely to get a better interest rate because the bank sees the loan as less risky.

-

Watch the “Document Fees”: In 2026, some dealers are charging upwards of $800 for “processing.” This isn’t part of the interest rate, but it adds to your total loan amount. Always ask for these to be reduced or removed.

Conclusion: Putting You in the Driver’s Seat

At the end of the day, finding the Best Auto Loan Rates in 2026 (Full Comparison) is about being a proactive consumer rather than a passive one. The dealership is a convenient one-stop-shop, but convenience usually comes with a hefty price tag. By taking the time to check with credit unions, looking into green energy incentives, and walking in with a pre-approval, you change the power dynamic.

Don’t let the monthly payment distract you from the total cost. Whether you end up with a 2% rate on a new EV or a 6% rate on a sturdy used truck, the goal is to ensure the car serves your life, not your debt. Take a deep breath, run your own simulations, and remember that the best deal is the one that fits into your long-term financial freedom. Happy hunting, and may your interest rates be low and your miles be plenty!