You’ve spent weeks researching the perfect car, comparing engine specs, and debating over the best interior color. You finally walk into the dealership, take a test drive, and fall in love. But as you sit down in that small, glass-walled office with the finance manager, the game shifts from mechanical engineering to financial maneuvering. Most people think the dealership’s primary goal is to sell cars, but the reality in 2026 is that the “F&I” (Finance and Insurance) office is often where the real profit is made. Understanding the gears turning behind that desk is the difference between getting a fair deal and paying a “hidden tax” on your new ride.

Dealer financing, often referred to as “indirect lending,” is a process where the dealership acts as a middleman between you and a network of banks or their own “captive” finance company. While it offers undeniable convenience, it is a system designed with multiple layers of potential profit for the dealer—often at the buyer’s expense. To navigate this successfully, you need to see the transaction through the eyes of the dealer. It’s not just about the car; it’s about the “paper” behind it. Let’s peel back the curtain on how these deals are structured and the psychological tricks used to nudge you into more expensive choices.

The Mechanic of the “Middleman”

When you apply for financing at a dealership, they aren’t usually lending you their own money. Instead, they send your credit profile to several lending partners. These banks look at your score and send back a “buy rate.” This is the actual interest rate the bank is willing to offer you based on your risk profile. However, you rarely see this number.

The dealer then adds a “markup” to that rate—often one or two percentage points—and presents you with the “contract rate.” This markup is pure profit for the dealership, often called a “dealer reserve.” In 2026, even as digital transparency has increased, this remains a standard practice. If the bank offers a 5% rate and the dealer tells you it’s 7%, that 2% difference over a 60-month loan can add thousands of dollars to your total cost without you ever realizing you had a better option.

The Psychological Playbook: The Four-Square and Beyond

Dealerships are masters of anchoring your attention where they want it. One of the most common “tricks” is focusing entirely on the monthly payment rather than the total price of the car or the interest rate. By shifting the conversation to “What can you afford per month?”, they gain the freedom to stretch out the loan term or hide expensive add-ons in the fine print.

The “Payment Packing” Trick

Payment packing occurs when a salesperson quotes you a monthly payment that is higher than what is actually required for the car and the interest rate. They then “fill” that extra room with products like paint protection, fabric guards, or extended warranties, making it seem like these items are “included” or only cost a few extra dollars a month. It’s a subtle way of making expensive upgrades feel insignificant.

The Yo-Yo Financing Trap

This is one of the more aggressive tactics, though it’s becoming rarer due to tighter regulations. In a “Yo-Yo” deal, the dealer lets you drive the car home under the impression that your financing is approved (“spot delivery”). A few days later, they call you back saying the financing “fell through” and you need to sign a new contract with a higher interest rate or a larger down payment. It preys on the emotional attachment you’ve already formed with the vehicle in your driveway.

Advantages and Disadvantages of Dealer Financing

It’s not all smoke and mirrors. There are legitimate reasons why millions of people choose this route every year.

Advantages

-

Unbeatable Convenience: You can choose a car, trade in your old one, and secure financing all in a single afternoon.

-

Manufacturer Incentives: “Captive” lenders like Ford Credit or Toyota Financial Services often offer 0% or 1.9% APR deals that traditional banks simply cannot match.

-

Flexibility for Lower Scores: Dealerships have relationships with “subprime” lenders who specialize in helping people with bruised credit get back on the road.

Disadvantages

-

Higher Interest Rates: Due to the markup mentioned earlier, you are almost always paying a higher rate than if you went directly to a credit union.

-

Pressure Tactics: The F&I office is a high-pressure sales environment where you are often tired and ready to leave, making you more likely to agree to things you don’t need.

-

Complex Contracts: Dealer contracts are often dense and filled with “junk fees” that can be difficult to spot in the moment.

Vale a pena? (Is it worth it?)

Is dealer financing worth it in 2026? The answer is a resounding “sometimes.” It is absolutely worth it if—and only if—you are qualifying for a manufacturer’s special promotional rate. If the brand is offering 0.9% APR to clear out inventory, no local bank will beat that. In that scenario, the dealership is actually losing money on the financing to move the metal.

However, if you are looking at a “standard” rate, dealer financing is rarely the smartest financial move. You are essentially paying a premium for the convenience of not having to visit your bank beforehand. For most buyers, that “convenience fee” ends up being far more expensive than a few hours of prep work would have cost.

O que considerar antes de escolher (What to consider before choosing)

To beat the dealer at their own game, you need to walk in with a shield. Consider these three factors before you even set foot on the lot:

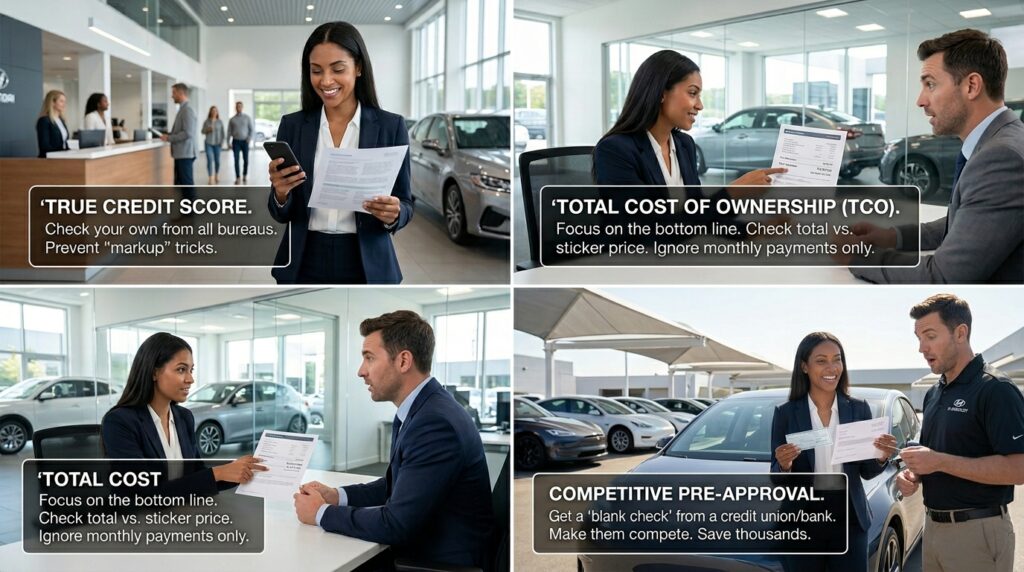

Your “True” Credit Score

Don’t rely on the dealer’s assessment. Check your own score across all three bureaus. Knowing exactly where you stand prevents the dealer from telling you your credit is “worse than you thought” as a justification for a higher interest rate.

The Total Cost of Ownership (TCO)

Ignore the monthly payment for a moment. Look at the “bottom line” on the contract. What is the total amount you will have paid after 60 or 72 months? If that number is 50% higher than the sticker price of the car, the financing deal is a bad one.

Competitive Pre-Approval

This is your ultimate leverage. Visit a credit union or an online lender and get a “blank check” pre-approval. When the dealer quotes you a rate, you can simply say, “My bank is giving me 5.2%. Can you beat that?” Suddenly, the dealer has to compete for your business, and that “markup” usually vanishes instantly.

Dicas importantes (Important tips)

To avoid the hidden tricks of dealer financing, follow these “insider” tips from the pros:

-

Negotiate the Car Price and the Finance Separately: Many people make the mistake of mixing them. Keep the price of the car as one negotiation and the interest rate as a completely separate conversation.

-

Beware the “Junk” Fees: Look for terms like “Documentation Fee,” “Electronic Filing Fee,” or “Market Adjustment.” Some are legitimate, but many are just extra profit. Ask the dealer to explain—and potentially remove—any fee that seems excessive.

-

Read the “Back-End” Products Carefully: GAP insurance, tire and wheel protection, and service contracts can be useful, but they are almost always cheaper if bought through a third party or your own insurance company.

-

The “No-Penalty” Clause: Ensure your loan has no “pre-payment penalty.” This allows you to refinance the loan with your own bank a month later if you realize the dealer gave you a bad rate.

Comparison: Dealer vs. Bank Financing

| Feature | Dealer Financing | Bank / Credit Union |

| Speed | Instant | 24-48 Hours |

| Rates | Often Marked Up | Usually Lower/Base Rate |

| Incentives | Access to 0% APR Promos | No Promo Rates |

| Relationship | Transactional | Built on History |

| Add-ons | Heavily Pushed | Rarely Offered |

The 2026 Digital Shift

In 2026, many dealerships have moved toward “digital retailing” tools on their websites. This is actually a win for the consumer. It allows you to play with the numbers, adjust your down payment, and see real interest rate estimates from the comfort of your couch without a salesperson looming over you. Use these online tools to build your “ideal deal” before you go in. It sets a baseline that is much harder for the dealer to manipulate once you arrive in person.

Conclusion

Understanding How Dealer Financing Really Works (Hidden Tricks Explained) isn’t about being cynical; it’s about being an informed consumer. The dealership is a business, and the F&I office is a profit center. There is nothing inherently wrong with a dealer making a profit, but you shouldn’t have to overpay for your loan just because you didn’t know the “buy rate” was lower.

The goal of your car-buying journey should be to drive away in a vehicle you love with a loan that doesn’t haunt your future. By getting pre-approved, focusing on the total price rather than the monthly payment, and being willing to say “no” to the high-pressure add-ons, you take the power back.

Dealer financing can be a great tool if used correctly—especially with those rare 0% APR offers. But for every other situation, your bank or credit union is likely your best friend. Do your homework, keep your eyes on the numbers, and remember: you are the one in the driver’s seat, both on the road and at the negotiating table. Safe driving!