Buying your first car is more than just a rite of passage; it’s a major financial milestone that sets the tone for your credit history and your future budget. In 2026, the market for first-time buyers has shifted. We are no longer in an era where you just find a “beater” for a few hundred dollars; today, a first car needs to be a balance of safety, modern technology, and—most importantly—smart financing.

For a beginner, the goal isn’t just to get from point A to point B. It’s to do so without becoming “car poor.” Financing your first vehicle allows you to build a credit profile, but it also carries risks if you choose the wrong car or a predatory loan.

In this guide, we’ll explore the best first cars to finance right now and the strategy you should use to ensure your first automotive investment is a success.

Why Your First Car Should Be a “Financial Bridge”

When you are starting out, your car serves as a bridge. It gets you to work, to school, and back home, but it also bridges your current financial status to your future one. A car that is too expensive to maintain or one that depreciates too quickly can burn that bridge.

The best first cars to finance are those that offer high reliability (so you aren’t paying for repairs and a car loan at the same time) and high resale value. If you decide to upgrade in three years, you want a car that still has significant equity.

Top Picks: The Best First Cars to Finance in 2026

We’ve selected these vehicles based on their safety ratings, fuel efficiency, and the “special” financing programs often available for first-time buyers.

1. The Toyota Corolla (The Gold Standard)

There is a reason the Corolla is the best-selling car in history. For a beginner, it is the safest financial bet you can make. In 2026, the Corolla comes standard with advanced safety suites that often lead to lower insurance premiums for young drivers.

From a financing perspective, Toyota Financial Services often has “College Graduate” or “First-Time Buyer” programs. These programs can help you secure a competitive interest rate even if your credit history is “thin.” Because Corollas hold their value so well, you are less likely to end up “underwater” on your loan.

2. The Honda Civic (The Value Retainer)

The Honda Civic is the Corolla’s fiercest rival, offering a bit more “personality” in its handling and design. It’s an excellent first car to finance because of its legendary longevity.

If you take out a 48 or 60-month loan on a Civic, there is a very high probability that the car will still be running perfectly long after the final payment is made. Financing a car that can easily last 15 years gives you the option to drive “payment-free” for a long time after the loan is settled.

3. The Mazda3 (The “Premium” Feel for Less)

If you want something that feels a bit more upscale without the luxury car price tag (or insurance costs), the Mazda3 is the winner. Mazda has moved significantly upmarket in recent years.

The reason it’s great for financing is that Mazda often offers aggressive APR incentives—sometimes as low as 0% or 1.9% for qualified buyers—to compete with the “big two” (Toyota and Honda). It’s a way to get a premium-feeling interior while staying within a mainstream budget.

4. The Subaru Impreza (For Tougher Climates)

If you live in a region with heavy snow or rain, the Subaru Impreza is the smartest first car to finance. It is the only car in its class that comes standard with Symmetrical All-Wheel Drive.

Subaru owners are incredibly loyal, which keeps used prices high. This means that if you finance an Impreza, your “collateral” remains valuable. Subaru also has excellent safety ratings, which is a major factor for parents helping their children navigate their first purchase.

Understanding the “First-Time Buyer” Loan

Financing a car for the first time is different than doing it the second or third time. Lenders view you as a higher risk because you don’t have a track record of making large monthly payments.

The Power of a Co-Signer

If you are a beginner with a low credit score or no credit history, your interest rate could be double what an experienced buyer pays. This is where a co-signer (usually a parent or guardian) comes in.

A co-signer with good credit “vouchers” for you. It allows you to get a much lower interest rate, saving you thousands of dollars over the life of the loan. Just remember: if you miss a payment, it hurts their credit score too.

The Down Payment: Your Shield Against Interest

For your first car, try to put down at least 10% to 20%. This does two things:

-

Reduces your monthly payment.

-

Shows the bank you are serious. A larger down payment makes the bank more likely to approve your loan at a lower rate.

Hidden Costs: It’s Not Just the Monthly Payment

Many beginners make the mistake of only looking at the loan payment. To be a “smart buyer,” you must calculate the Total Monthly Cost.

Insurance for Beginners

Insurance for first-time drivers is expensive. Before you finance a car, get an insurance quote for that specific VIN. A “sporty” car might have a $400 monthly payment but a $300 insurance bill, whereas a compact SUV might have a $450 payment but only $150 for insurance. Always look at the “all-in” number.

Maintenance and Fuel

Electric vehicles (EVs) are becoming popular first cars because of low maintenance, but if you can’t charge at home, the “convenience cost” might be high. Conversely, an older used luxury car might be cheap to buy, but one single repair could cost more than three months of loan payments. Stick to the reliable “commuter” brands for your first finance.

New vs. Used: Which Should a Beginner Finance?

This is the age-old question. In 2026, the answer depends on the interest rates.

The Case for New

Often, manufacturers offer special APRs (like 1.9%) on new cars but not on used ones. If you finance a $25,000 new car at 1.9%, your monthly payment might be almost the same as a $21,000 used car financed at 8.5%. Plus, the new car comes with a full warranty, meaning your monthly budget is protected from surprise repair bills.

The Case for Used

A used car (especially a 2–3 year old lease return) has already taken its biggest depreciation hit. If you can find a low-interest loan through a credit union, a used car is a great way to keep your total debt lower. Just make sure to get a Pre-Purchase Inspection (PPI) so you aren’t financing someone else’s problems.

How to Avoid Common Beginner Mistakes

-

Don’t Finance the “Fun” Extras: Dealerships will try to add window tinting, “protection packages,” and extended warranties into your loan. For a first car, skip these. They inflate your loan and you end up paying interest on things that don’t add real value to the car.

-

Keep the Term Short: It’s tempting to take an 84-month loan to get a $300 payment. Don’t do it. You’ll be “upside down” (owing more than the car is worth) for years. Aim for 48 or 60 months.

-

Read the Fine Print on “No Credit” Deals: If a lot says “We Finance Anyone,” the interest rates are likely predatory (20% or higher). You are better off buying a cheaper car for cash than signing a 25% interest rate loan.

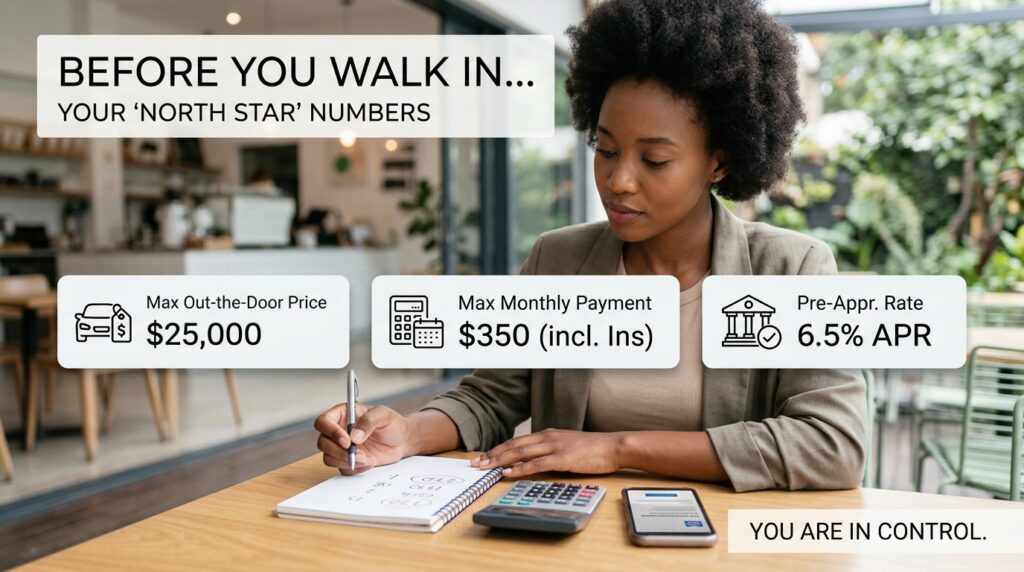

Preparing for the Dealership

Before you walk in, have your “North Star” numbers ready:

-

Your Max Out-the-Door Price.

-

Your Max Monthly Payment (including insurance).

-

Your Pre-Approved Interest Rate from a bank.

When you have these three numbers, the salesperson can’t “fudge” the math to make a bad deal look good. You are in control.

Final Thoughts

Your first car is a tool for freedom, but your first car loan is a tool for financial growth. By choosing a reliable, high-value vehicle like a Corolla or a Civic and financing it responsibly, you are doing more than just buying a ride—you are building a foundation for your future financial life.

Take your time, do the math, and don’t be afraid to walk away if the numbers don’t feel right. The best first car is the one that makes you smile when you drive it and keeps you relaxed when you check your bank account.

Happy driving, and welcome to the world of smart car ownership!