Have you ever wondered what actually happens behind the scenes after you click “submit” on a loan application? It used to be that a local banker who knew your family would look over your paperwork, shake your hand, and give you a nod of approval. Today, the process feels more like a black box. You send your data into the digital void, and minutes later, a verdict appears on your screen. In 2026, the way financial institutions look at you has shifted dramatically. They aren’t just looking at your bank balance anymore; they are looking at the “digital shadow” you leave behind. Understanding this evolution is the only way to ensure you stay on the right side of the approval line.

If you’ve been following the financial news lately, you know that the “old rules” of credit are being rewritten. The basic three-digit credit score still matters, of course, but it’s no longer the only player on the field. When we talk about How Banks Evaluate Your Risk in 2026, we are talking about a multi-dimensional analysis that includes everything from your real-time spending habits to the stability of your industry. Banks have become incredibly protective of their capital, and they use highly sophisticated models to predict your behavior years into the future. It sounds intimidating, but once you pull back the curtain, you’ll realize that these systems actually reward transparency and consistency. Let’s dive into the new mechanics of risk assessment.

Beyond the FICO Score: The Rise of Holistic Data

For decades, the FICO score was the beginning and the end of the conversation. Today, it’s just the cover of the book. In 2026, banks are increasingly moving toward “Holistic Underwriting.” This means they are looking at the context of your life, not just your payment history. They want to see the “flow” of your money. Are you someone who saves a small amount every single month, or are you someone who gets a big windfall and spends it all in a weekend?

This shift has led to the adoption of “Open Banking” protocols. When you apply for a loan now, you are often asked to securely link your bank account. The lender’s software then analyzes your transactions. They look for “lifestyle markers”—consistent rent payments, regular utility bills, and even how often you use high-interest “Buy Now, Pay Later” services. If you have a 700 credit score but you’re constantly overdrawing your checking account, the bank will see you as a high risk. Conversely, a 640 score with a perfectly managed checking account might get a “yes” because the real-time data shows responsible behavior.

Industry Stability and Career Pathing

Another massive shift in 2026 is how lenders evaluate your employment. It used to be enough to just have a job. Now, banks look at the “viability” of your career path. With the economy shifting rapidly due to automation and changing consumer habits, some industries are flagged as higher risk than others. A software developer at a stable firm is viewed differently than a worker in a declining manufacturing sector, even if they earn the same salary.

Lenders are also looking at your “Income Consistency.” For the millions of people in the gig economy or running freelance businesses, the evaluation has changed. Instead of just looking at last year’s tax return, banks are looking at your 24-month rolling average. They want to see that your income isn’t just a fluke. If you can show that you’ve maintained a steady income across different clients or platforms, you are no longer seen as a “risky freelancer”—you are seen as a resilient entrepreneur.

The “Social Stability” Factor

This is where things get a bit more subtle. While banks don’t officially “stalk” your social media, they do use public data to verify the facts on your application. If you claim to live in a certain city but your digital footprint (like registered addresses or utility connections) shows you elsewhere, it triggers a fraud alert.

Stability is the ultimate goal for a lender. They look for “longitudinal data”—how long you’ve had the same phone number, how long you’ve been at your current address, and how long you’ve been with your employer. In 2026, a “digital nomad” lifestyle might be great for your soul, but it’s a nightmare for a risk algorithm. The more “rooted” you appear in your digital data, the lower your risk profile becomes.

Worth It?

Is it worth it to play along with these new, intrusive evaluation methods? For many, the idea of linking a bank account feels like a violation of privacy. However, you have to weigh that against the “Credit Gap.” If you have a “thin” credit file or you’re a young person just starting out, traditional credit scores will almost always fail you.

In my experience, opting into these newer evaluation methods is worth it because it provides a more accurate picture of who you are as a person. If you are a responsible spender but don’t like using credit cards, “Open Banking” is the only way to prove to a bank that you are a safe bet. It levels the playing field for people who don’t fit the traditional 1950s-era financial mold. In 2026, transparency is the price of admission for fair interest rates.

What to Consider Before You Apply

Before you let a bank run your data through their 2026 risk model, you need to consider three critical things that could make or break your deal:

Your “Digital Hygiene”

Take a look at your bank statements from the last 90 days. If a stranger looked at them, what would they think? Are there constant transfers to gambling sites? Are you paying $200 a month in “late fees” to various apps? Clean up your transactions for three months before applying. Make your bank statement look like the most boring document on earth.

The “Debt-to-Income” Ceiling

Even with all the new data, the old math of DTI (Debt-to-Income) still has a hard ceiling. Most banks in 2026 will not exceed a 45% DTI. If you have a lot of “invisible” debt—like small monthly payments for furniture, tech gadgets, or clothing—add them up. They count against your risk. Pay off as many of those “micro-debts” as possible to clear space for a car loan or mortgage.

The Timing of Your Career Moves

If you are planning to change jobs, do not do it right before applying for a loan. Even if the new job pays more, the “reset” of your tenure clock is a massive risk signal. Banks in 2026 value “tenure” more than “potential.” Secure your financing while you still have your longest-running job on your resume.

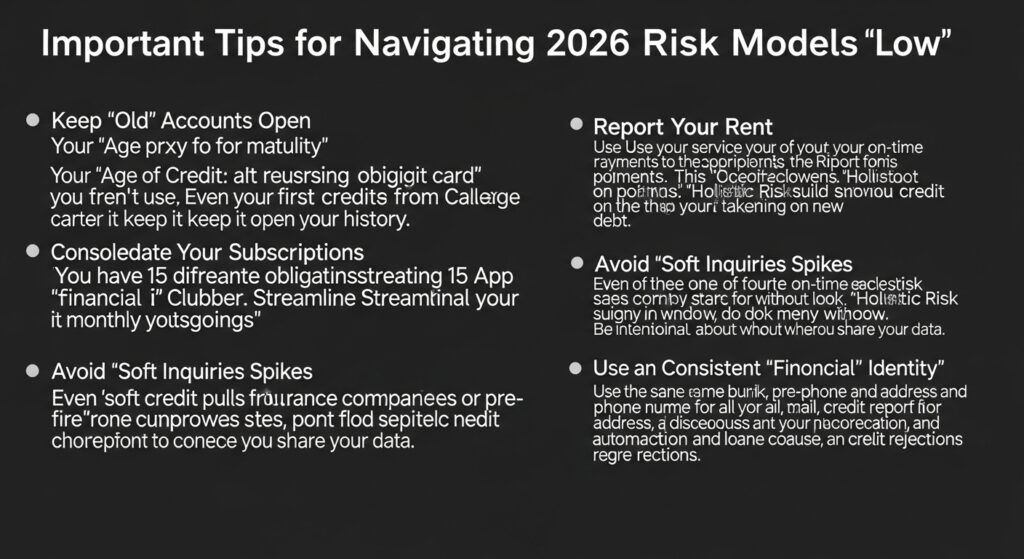

Important Tips for Navigating 2026 Risk Models

If you want to stay ahead of the curve and ensure your risk profile remains “Low,” keep these tips in mind:

-

Keep “Old” Accounts Open: Your “Age of Credit” is a proxy for maturity. Even if you don’t use your first credit card from college, keep it open. It anchors your history.

-

Consolidate Your Subscriptions: In 2026, lenders look at “recurring obligations.” If you have 15 different streaming and app subscriptions, it looks like “financial clutter.” Streamline your monthly outgoings.

-

Report Your Rent: Use a service that reports your on-time rent payments to the credit bureaus. This is one of the easiest ways to build “Holistic Risk” points without taking on new debt.

-

Avoid “Soft” Inquiries Spikes: Even “soft” credit pulls from insurance companies or “pre-approval” sites can start to look suspicious if you do too many in a short window. Be intentional about where you share your data.

-

Use a Consistent “Financial Identity”: Use the same email, phone number, and address for all your financial accounts. Discrepancies between your bank, your credit report, and your loan application are the #1 cause of “automated rejections.”

The 2026 Perspective: Fraud Detection vs. Risk Assessment

It’s important to distinguish between being a “risk” and being “flagged for fraud.” In 2026, many rejections aren’t because the person has bad credit, but because the bank’s system couldn’t verify their identity to a 99% certainty. With the rise of synthetic identity theft, banks are on high alert. If you’ve recently moved or changed your name, make sure every single piece of your digital life—from your Amazon account to your LinkedIn to your bank—is updated. A single mismatched data point can kill an approval faster than a 500 credit score.

Conclusion

Understanding How Banks Evaluate Your Risk in 2026 is about realizing that you are no longer just a number; you are a narrative. Your financial life is a story told through thousands of data points, and your job is to make sure that story is one of stability, growth, and responsibility.

The “black box” of lending doesn’t have to be scary. In fact, for the disciplined borrower, the new models offer more opportunities than ever to get fair rates and fast approvals. By maintaining good digital hygiene, keeping your employment stable, and being transparent with your cash flow data, you can navigate the 2026 lending landscape with total confidence.

The world of finance will continue to evolve, but the core principles remain the same: show the bank that you are a person of your word, and that your future is just as bright as your past. Take control of your data today, and the “Approved” screen will be waiting for you tomorrow. Safe travels on your financial journey!