When you start shopping for a vehicle in 2026, the sheer volume of financial jargon thrown your way can be overwhelming. You’ll hear about APRs, residuals, and amortization schedules, but the most fundamental fork in the road is often ignored until the final paperwork is being drawn up: Are you getting a Secured or an Unsecured car loan?

It might sound like a minor technicality, but this distinction changes everything. It dictates your interest rate, how much you can borrow, and—most importantly—what happens if life takes an unexpected turn and you can’t make your payments.

In this guide, we’re going to strip away the bank-speak and give you a real-world breakdown of these two lending paths. Whether you’re looking at a brand-new EV or a reliable used sedan, understanding the “Security” of your loan is the first step toward a truly smart purchase.

What Is a Secured Car Loan? (The Industry Standard)

The vast majority of car loans in 2026 are secured loans. In this arrangement, the car you are buying acts as collateral for the debt. Think of it like a mortgage for your house: the lender “owns” a stake in the asset until the final penny is paid off.

Because the bank has something they can physically take back and sell to recover their money if you stop paying, they view this as a low-risk transaction. This lower risk for the bank usually translates into better terms for you.

How the “Lien” Works

When you take out a secured loan, the lender places a lien on the vehicle’s title. You are the registered owner, but the bank holds the title or is listed as the primary lienholder. Once you make that very last payment, the lender releases the lien, and the car becomes yours “free and clear.”

If you fail to make payments, the “secured” nature of the loan gives the lender the legal right to repossess the car. In many states, they don’t even need a court order to do this; they can simply send a tow truck to your driveway.

What Is an Unsecured Car Loan? (The “Signature” Loan)

An unsecured car loan is a different beast entirely. In this scenario, the bank gives you the money based solely on your creditworthiness and your promise to pay it back. There is no collateral. The car’s title is in your name from day one, and the bank has no direct claim to it.

These are often called “personal loans” or “signature loans.” Because the bank has no physical asset to seize if you disappear, they are taking a much higher risk. To compensate for that risk, they charge more.

Why Would Anyone Choose This?

You might wonder why anyone would opt for an unsecured loan if it’s more expensive. The answer usually lies in the vehicle’s age or the buyer’s desire for flexibility. Traditional secured loans often have “year” and “mileage” caps (e.g., they won’t finance a car older than 10 years).

An unsecured loan allows you to buy a classic car, a high-mileage work truck, or even a car from a private seller without the bank’s “approval” of the vehicle itself. You are borrowing the money, not “mortgaging” the car.

Interest Rates: The Price of Security

In 2026, the gap between secured and unsecured interest rates is significant. Since the bank has the safety net of the car in a secured loan, they can offer much lower APRs.

If you have great credit, you might see a secured loan at 5% or 6%. For that same buyer, an unsecured personal loan might start at 11% or 12%. Over a 60-month term on a $25,000 car, that interest gap can cost you thousands of dollars in extra payments.

The Impact on Your Monthly Budget

Choosing an unsecured loan simply because “I want the title in my name” is often a poor financial move for a standard car purchase. You are effectively paying a premium for a psychological benefit. Unless the car is too old for traditional financing, a secured loan is almost always the more “budget-friendly” option for your monthly cash flow.

Credit Score Requirements

Because there is no collateral to fall back on, unsecured loans have much higher barriers to entry. To get a large unsecured loan for a vehicle, you typically need an “Excellent” credit score (usually 720 or higher) and a very low debt-to-income ratio.

Secured loans are much more accessible for “Fair” or “Good” credit scores. Because the car exists as a backup for the bank, they are willing to work with people who have had a few bumps in their financial history. If you are rebuilding your credit, a secured car loan is often one of the best ways to get back on track.

Insurance Requirements: The “Full Coverage” Mandate

One hidden cost of a secured loan is the insurance requirement. Since the bank owns the car as collateral, they want to make sure their “investment” is protected from accidents, theft, or natural disasters.

The lender will mandate that you carry “Full Coverage” insurance (Comprehensive and Collision) with a specific deductible (usually $500 or $1,000). If you were planning on only carrying “Liability” insurance to save money, a secured loan will prevent you from doing that.

The Freedom of Unsecured Loans

With an unsecured loan, the bank doesn’t care what kind of insurance you have because they don’t care about the car. You could, theoretically, carry only the state-mandated minimum liability. While we never recommend this (if you crash the car, you still owe the full loan amount even if the car is scrap), it does give you more control over your monthly insurance expenses.

What Happens During a Default?

This is the “worst-case scenario” section, but it’s the most important one to understand before you sign a contract.

Secured Loan Default: The Repossession

If you default on a secured loan, the bank takes the car. They sell it at an auction. If they sell it for $15,000 but you owed $18,000, you are still responsible for that $3,000 “deficiency balance.” Your credit score will take a massive hit, and you will be without transportation.

Unsecured Loan Default: The Legal Route

If you default on an unsecured loan, the bank cannot take your car immediately. However, that doesn’t mean you’re off the hook. They will send the debt to a collection agency, sue you in court, and potentially garnish your wages or put a lien on your home. It is a slower process than repossession, but it can be even more destructive to your long-term financial health.

Financing From Private Sellers

In 2026, many of the best deals are found in private driveways, not on dealer lots. However, financing a private sale with a secured loan can be a logistical headache. The bank has to verify the seller’s title, ensure there are no other liens, and often handle the title transfer themselves.

This is where the unsecured loan shines. The bank simply deposits the cash into your account. You go to the seller, hand them the money, and they give you the car and the title. It’s as simple as a cash deal. If you value speed and want to buy from an individual, the convenience of an unsecured loan might outweigh the higher interest rate.

The “Negative Equity” Factor

Negative equity (being “underwater”) is a major risk with secured loans. Because you are often financing the taxes, fees, and the car’s full value, you might owe more than the car is worth for the first few years.

In an unsecured loan, the concept of “negative equity” doesn’t really exist in the same way because the loan isn’t tied to the car’s value. However, the financial reality is the same: if you sell the car for $10,000 but still owe $15,000 on your personal loan, you still have to come up with that $5,000 gap out of your own pocket.

Which One Should You Choose?

To make the “Smart” choice, you have to look at your specific situation through an objective lens.

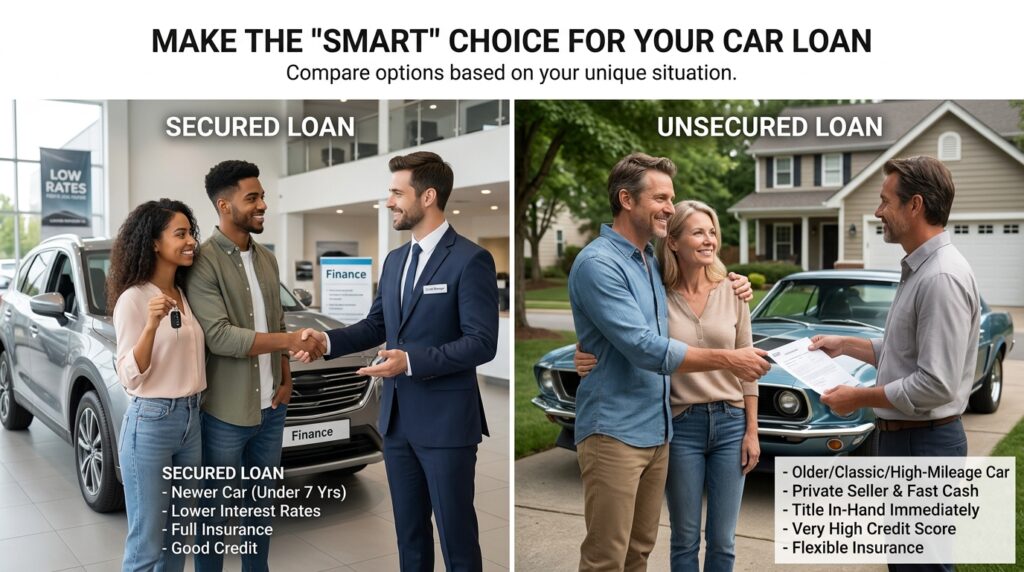

Choose a Secured Loan if:

-

You are buying a new or late-model used car (under 7 years old).

-

You want the lowest possible interest rate.

-

You already plan on carrying full-coverage insurance.

-

You have “Good” but not “Perfect” credit.

Choose an Unsecured Loan if:

-

You are buying an older “high-mileage” car or a classic vehicle.

-

You are buying from a private seller and want a fast, “cash-like” transaction.

-

You have a very high credit score and value the convenience of having the title in your name immediately.

-

You want the flexibility to choose your own insurance levels to save on monthly costs.

Final Thoughts: The “Real World” Advice

For 90% of buyers in 2026, the Secured Car Loan is the superior choice. The interest savings alone are usually enough to justify the extra paperwork and the insurance requirements. Paying 5% interest versus 12% interest can be the difference between a car that helps you build wealth and a car that keeps you in a cycle of debt.

However, the “Smart” part of buying is knowing that options exist. If you find a perfect 2012 truck that a bank won’t touch with a traditional loan, knowing how to leverage an unsecured personal loan can help you secure a reliable vehicle that fits your life.

Before you sign any loan document, ask the lender: “Is this loan secured by the vehicle?” If they say yes, make sure you’re getting the low interest rate that comes with that security. If they say no, make sure you understand exactly how much extra you’re paying for that freedom. Knowledge is your best leverage in the finance office.