Have you ever sat in a bank office or scrolled through a lending app, only to find yourself mesmerized by the “monthly payment” figure? It’s a classic move. Lenders love to show you how a $30,000 loan can cost “only” $400 a month. It feels like a win, right? But there is a hidden lever moving behind those numbers that most people ignore until it’s too late. That lever is time. The longer you take to pay back a debt, the more the math shifts in favor of the bank and away from your savings account.

Understanding the relationship between Loan Term vs Interest Paid: Full Breakdown is arguably the most important step in financial literacy. It’s the difference between buying a car and buying a car plus a luxury vacation for your banker. In the economic landscape of 2026, where interest rates have regained their bite, the length of your loan isn’t just a detail—it’s the primary factor determining your total net worth over the next decade. Let’s pull back the curtain on how time inflates your debt and how you can fight back.

The Compounding Trap of Time

When we talk about interest, we often focus on the percentage rate (the APR). While that matters, the “term”—or the duration of the loan—is what actually dictates how many times that percentage gets applied to your balance. Every month that you carry a balance, the bank calculates interest. If you stretch a 3-year loan into a 6-year loan, you aren’t just doubling the time; you are radically increasing the total “rent” you pay for that money.

Most people view a longer term as a way to “afford” something they otherwise couldn’t. But this is a dangerous psychological trick. A lower monthly payment isn’t a discount; it’s an expensive extension. By the time you reach the end of a long-term loan, you might find that the interest paid has actually eclipsed the original value of the item you bought.

The Math in Action: A $40,000 Simulation

Let’s look at a practical, real-world scenario. Imagine you are financing a high-quality SUV for $40,000 at a fixed interest rate of 7%. Most buyers today are offered terms ranging from 36 to 84 months. Let’s see what happens to your wallet in each case.

Option A: The “Aggressive” 36-Month Term

-

Monthly Payment: ~$1,235

-

Total Interest Paid: ~$4,450

-

Total Cost of Car: $44,450

Option B: The “Standard” 60-Month Term

-

Monthly Payment: ~$792

-

Total Interest Paid: ~$7,520

-

Total Cost of Car: $47,520

Option C: The “Extended” 84-Month Term

-

Monthly Payment: ~$604

-

Total Interest Paid: ~$10,750

-

Total Cost of Car: $50,750

The Breakdown: By choosing the 84-month term over the 36-month term, you “saved” $631 every month in cash flow. However, you paid an extra $6,300 in interest. That is a massive penalty for the convenience of a lower payment. In Scenario C, you are essentially paying for a whole extra year of car payments that go strictly to the bank’s profit margin, not toward the car itself.

The “Upside Down” Danger

There is a technical risk to long loan terms that many people don’t realize until they try to sell their asset: depreciation. Most things we finance—cars, electronics, furniture—lose value the moment we take them home.

When you have a 72 or 84-month loan, you are paying off the principal balance so slowly that the car’s value often drops faster than the loan balance. This is called being “underwater” or “upside down.” If you get into an accident or need to sell the car in year three, you might find you owe the bank $25,000 for a vehicle that is only worth $18,000. A shorter loan term is your best defense against this financial nightmare.

Is it Worth It?

Is it ever worth taking the longer term? In the context of Loan Term vs Interest Paid: Full Breakdown, the answer is a nuanced “sometimes,” but only for specific reasons.

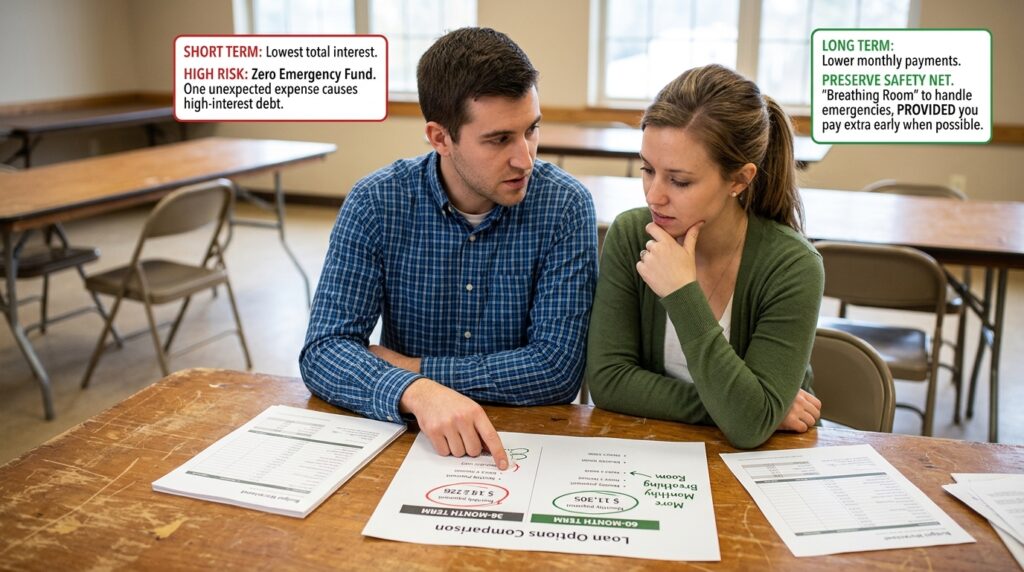

If taking a 36-month loan means you have zero money left for an emergency fund, it’s not worth the risk. One medical bill or a home repair could force you into high-interest credit card debt, which is far worse than a slightly longer car loan.

In this case, it is “worth it” to take the 60-month loan to preserve your monthly “breathing room,” provided you have the discipline to pay it off early when you have extra cash. The goal should be to find the shortest term that you can comfortably afford without sacrificing your safety net.

What to Consider Before You Choose

Before you let a salesperson convince you that “only $300 a month” is a great deal, run through this mental checklist:

1. The Asset’s Lifespan

Never finance something for longer than its useful life. If you are financing a laptop for 5 years, but the laptop will be obsolete in 3, you are paying for a ghost. Always ensure the “Loan Term vs Interest Paid” math aligns with how long the product will actually serve you.

2. Your Career Stability

A long-term loan is a bet on your future income. Can you guarantee you’ll have that same paycheck 7 years from now? Shorter terms give you more flexibility to pivot your life because you’ll own your assets outright much sooner.

3. Prepayment Clauses

In 2026, some lenders include “hidden” penalties if you try to pay the loan off early. They want that interest money! Always ask: “If I win the lottery tomorrow and pay this off, is there a fee?” If the answer is yes, find a different lender.

Important Tips

-

The “Half-Payment” Strategy: If you must take a longer term for safety, try making your payments every two weeks instead of once a month. You’ll end up making one extra full payment every year, which can shave months off a 5-year loan and save you hundreds in interest.

-

Focus on Total Out-the-Door Cost: When negotiating, ignore the monthly payment. Ask the seller for the “Total Cost of the Loan” including all interest over the full term. It’s a sobering number that often changes a buyer’s mind instantly.

-

The 20% Rule: Try to put 20% down in cash. This lowers the amount you need to finance, which naturally reduces the total interest paid regardless of the term you choose.

-

Refinance Later: If you are stuck in a long-term, high-interest loan now, keep a close eye on your credit score. If it improves, you can often refinance into a shorter, lower-interest loan and save your future self a fortune.

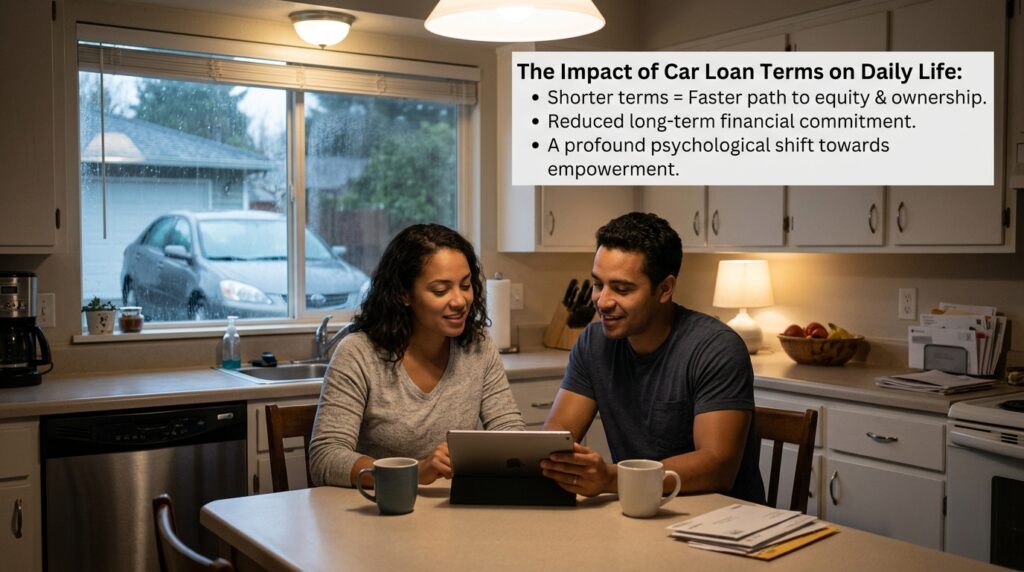

The Psychological Weight of Debt

We often talk about these numbers as if they exist in a vacuum, but they affect your daily stress levels. A 7-year car loan is a 7-year commitment to a bank. That’s a long time to have a “must-pay” item on your list every single month.

I’ve noticed that people who choose shorter terms tend to feel more empowered in their financial lives. They reach “equity” faster, meaning they actually own a portion of the asset. There is a profound psychological shift that happens when you realize you are working for yourself, rather than working to pay off a decision you made five years ago.

Conclusion: Mastering the Clock

In the battle of Loan Term vs Interest Paid: Full Breakdown, time is either your greatest ally or your most expensive enemy. If you treat a loan like a short-term tool to get what you need, you’ll come out ahead. If you treat it like a way to live a lifestyle you haven’t yet earned, the interest will slowly erode your financial foundation.

Always aim for the shortest term your budget can handle. Look past the small monthly numbers and focus on the big “Total Interest” figure. If that number makes you uncomfortable, it’s a sign that the loan is too long.

The goal of personal finance isn’t just to have nice things; it’s to have nice things and keep your money. By mastering the clock and choosing shorter loan terms, you ensure that your hard-earned cash stays where it belongs—working for your future, not the bank’s bottom line. Make the smart choice today, and your future self will have much more to show for it.