Imagine walking into a dealership and falling in love with a high-end luxury sedan or a rugged, tech-heavy SUV. You look at the sticker price, run the numbers for a traditional loan, and realize the monthly payment is roughly the size of a modest mortgage. Just as you’re about to walk away, the finance manager leans in and offers a deal that seems almost too good to be true: a monthly payment that is significantly lower—sometimes by half—than the standard rate. The catch? A “balloon” waiting for you at the end of the road. In 2026, where monthly cash flow is king, this specific type of financing has seen a massive resurgence, but it remains one of the most misunderstood tools in the financial shed.

A balloon payment car loan is essentially a hybrid between a traditional purchase and a lease. While it allows you to drive a much nicer car for a smaller monthly check, it requires a strategic mindset and a clear exit plan. If you aren’t careful, that “balloon” can pop, leaving your finances in a precarious position. However, for the right driver with the right plan, it can be a brilliant way to leverage credit and maintain liquidity. Let’s dive deep into the mechanics of how these loans work today and whether you should consider signing on the dotted line.

How the “Balloon” Actually Works

To understand a balloon payment car loan, you have to visualize how a normal loan is paid off. In a standard setup, you pay down the principal and interest until the balance hits zero. With a balloon loan, you aren’t paying off the whole car. Instead, you agree to pay off a portion of the car’s value over a set term—say, three or four years—and leave a large “lump sum” (the balloon) for the very last payment.

This lump sum is usually based on the projected future value of the vehicle. Because you aren’t chipping away at that final chunk of debt every month, your monthly installments stay remarkably low. It’s like you’re only paying for the depreciation of the car during the time you’re driving it, plus interest on the total amount borrowed. It’s a deferred debt structure that prioritizes your immediate monthly budget over long-term equity.

The Attraction: Why People Choose Balloon Loans in 2026

In today’s economy, flexibility is a highly valued commodity. Many professionals prefer to keep more cash in their high-yield savings accounts or investment portfolios rather than tying it up in a depreciating metal asset sitting in their driveway.

Lower Monthly Commitment

The primary draw is, and always will be, the monthly payment. For a $60,000 vehicle, a standard 60-month loan might cost you over $1,100 a month. A balloon loan for the same car might drop that payment to $600 or $700. This lower barrier to entry allows people to afford safer, more modern, and more reliable vehicles that might otherwise be out of reach.

Driving More Car for Less

Balloon payments are especially popular in the luxury car segment. Manufacturers like BMW, Mercedes, and Audi have mastered this model because they know their customers often want to trade in for the newest model every few years. By using a balloon structure, the driver enjoys the premium experience during the car’s “golden years” without the heavy monthly burden of a full purchase.

Business Use and Tax Strategies

For entrepreneurs and freelancers, a balloon payment can be a tactical move. If you use the car for business, the lower monthly payments can help keep your business overhead low, while the final balloon payment can sometimes be timed with a projected year-end bonus or a specific business milestone.

The Risks: What Could Go Wrong?

If it sounds like a dream, remember that every financial shortcut has a shadow side. The biggest risk of a balloon payment car loan is the “End-of-Term Shock.”

The Interest Trap

Because you aren’t paying down a large portion of the principal, you are paying interest on that large “balloon” amount for the entire life of the loan. This means that by the time you reach the end of the contract, you will have paid significantly more in total interest than you would have with a traditional loan. You are essentially paying for the privilege of deferring your debt.

Negative Equity and Market Volatility

The balloon payment is calculated based on what the bank thinks the car will be worth in three or four years. But what if the market shifts? If a new battery technology makes your 2026 EV obsolete by 2030, or if you get into an accident that lowers the car’s resale value, you might find yourself owing a $20,000 balloon payment on a car that is only worth $15,000. This is known as being “underwater,” and it’s a difficult hole to climb out of.

Your Options at the End of the Road

One of the coolest—and most stressful—parts of a balloon loan is the “Final Choice.” When that last month arrives and the balloon is due, you typically have three paths to choose from:

-

Pay It Off: You write a check for the full lump sum and the car is officially yours. This is the cleanest option if you have the cash saved up.

-

Refinance: If you don’t have the cash, most lenders will allow you to turn that balloon payment into a new, traditional loan. However, you’ll be paying interest on that money for a second time, often at a higher “used car” rate.

-

Sell or Trade-In: You sell the car or trade it back to the dealership. Ideally, the car is worth more than the balloon payment, and you can use that “profit” as a down payment on your next vehicle. If it’s worth less, you’ll have to pay the difference out of pocket.

Vale a pena? (Is it worth it?)

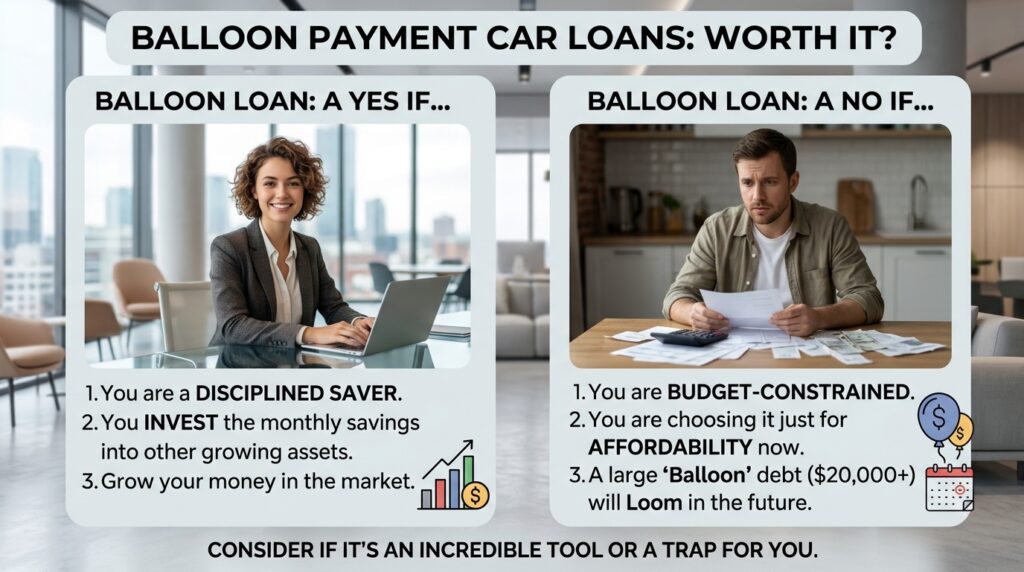

Determining if a What Is a Balloon Payment Car Loan and Is It Worth It? question leads to a “yes” depends entirely on your financial discipline.

If you are a disciplined saver who plans to take the money you “saved” on monthly payments and invest it elsewhere, this loan can be an incredible tool. You get to use the bank’s money to drive a car while your own money grows in the market.

On the other hand, if you are choosing a balloon loan because it’s the only way you can afford that specific car, you are likely playing a dangerous game. If you are living paycheck-to-paycheck with a $20,000 debt “balloon” looming three years in the future, you are setting yourself up for a financial crisis. In my experience, this loan is worth it for the strategically wealthy, but a potential trap for the budget-constrained.

O que considerar antes de escolher (What to consider before choosing)

Before you sign that contract, you need to look at more than just the monthly number. Here is what you should evaluate:

Your Future Income Stability Do you expect to be making more money in three or four years? A balloon loan “backloads” your financial responsibility. If your industry is volatile or you’re planning on retiring soon, a traditional loan with a predictable path to zero is much safer.

Mileage and Wear Just like a lease, the value of your car at the end of the term depends on its condition. If you drive 25,000 miles a year or tend to be “hard” on your vehicles, your trade-in value will plummet. This makes the final balloon payment much harder to cover through a sale or trade.

Current Interest Rates In a high-interest environment, balloon loans are more expensive because you’re carrying a larger balance for longer. In 2026, we’ve seen rates stabilize, but it’s still vital to calculate the Total Cost of Ownership (TCO) over the entire life of the loan.

Dicas importantes (Important tips)

If you’ve decided to go the balloon route, here are some pro tips to keep you safe:

-

Always Check the “Gap”: Ensure you have GAP insurance. If your car is totaled early in the loan, the insurance company will only pay the market value, which might be thousands of dollars less than what you owe on your balloon-heavy loan.

-

The “Side Savings” Account: Treat the balloon loan like a traditional loan. Take the difference between the “balloon” payment and a “normal” payment and put it into a dedicated savings account. If you do this, you’ll have the cash ready to pay off the balloon when it’s due.

-

Negotiate the Residual: Don’t just accept the bank’s first offer on the balloon amount. Sometimes there is room to negotiate the estimated future value, which can change your monthly math.

-

Read the “Refinance” Clause: Check if the contract guarantees you the right to refinance the balloon at the end. Some predatory loans don’t, which could force you to sell the car even if you don’t want to.

Balloon Loan vs. Leasing: The 2026 Comparison

Many people ask: “Why not just lease?” The difference is in ownership and flexibility. With a lease, you have a hard limit on miles and you generally must return the car. With a balloon loan, you are the owner. You can modify the car, drive as much as you want (though it affects resale), and you have the right to keep it forever if you choose.

In the 2026 market, balloon loans have become the preferred choice for people who want the “lower payments” of a lease but want to avoid the “rental” feel of a lease. It gives you the option to be an owner without the immediate cash-flow penalty of a traditional purchase.

The Technological Factor: EVs and Balloons

We cannot talk about car loans in 2026 without mentioning Electric Vehicles. The technology is moving so fast that a car’s value can drop significantly when a new, longer-range battery hits the market. If you are financing an EV with a balloon payment, be very conservative with the projected future value. You don’t want to be stuck with a massive balloon payment for a car that has been made obsolete by the next generation of solid-state batteries.

Conclusion

The question of What Is a Balloon Payment Car Loan and Is It Worth It? doesn’t have a simple yes or no answer. It is a sophisticated financial product that offers a “buy now, pay most of it later” lifestyle. For the savvy driver who understands their cash flow and has a plan for that final lump sum, it is a gateway to driving a premium vehicle while keeping their capital liquid.

However, for the unwary, it is a ticking clock. If you enter into a balloon loan, do so with your eyes wide open. Calculate the total interest, plan for the final payment from day one, and always have a Plan B in case the car’s value drops. Car ownership should be a source of freedom, not a source of looming dread. Use the balloon to your advantage, but never let it catch you by surprise.

In the end, the best loan is the one that aligns with your lifestyle today and your goals tomorrow. If you value low monthly costs and have the discipline to handle a future lump sum, the balloon might just be the lift your automotive dreams need. Happy driving!