We have all been there—sitting across from a loan officer or staring at a digital dashboard, watching the numbers dance around. One offer looks incredible with a low monthly payment, while the other seems a bit steeper but boasts a much lower interest rate. It’s easy to get tunnel vision and only focus on what is leaving your bank account this month. However, the difference between a high interest and a low interest loan isn’t just a couple of percentage points; it is the difference between buying one car and accidentally paying for one and a half.

Interest is essentially the “rent” you pay to use someone else’s money. In the current 2026 financial climate, where rates have been a bit of a roller coaster, understanding the High Interest vs Low Interest Loans: Real Impact is more vital than ever. It’s not just about the math on the page; it’s about your freedom, your future savings, and how much of your hard-earned paycheck stays in your pocket versus going into a bank’s skyscraper fund. Let’s peel back the layers and see what these numbers actually do to your life over the long haul.

The Anatomy of Interest: More Than Just a Number

To truly understand the impact, we have to look at how interest compounds and eats away at your principal. Most people think a 10% interest rate is just “a little worse” than a 5% rate. Mathematically, it feels linear. But in the world of amortized loans—the kind you get for cars or homes—that 5% gap can lead to a massive explosion in total cost.

When you take out a loan, your first few years of payments are heavily weighted toward interest. If your rate is high, you are barely touching the actual balance of the loan for a long time. This is why some people feel like they’ve been paying for years but still owe almost the full amount. A low interest loan, by contrast, starts attacking the principal balance much sooner. This “equity building” is the secret sauce to financial health.

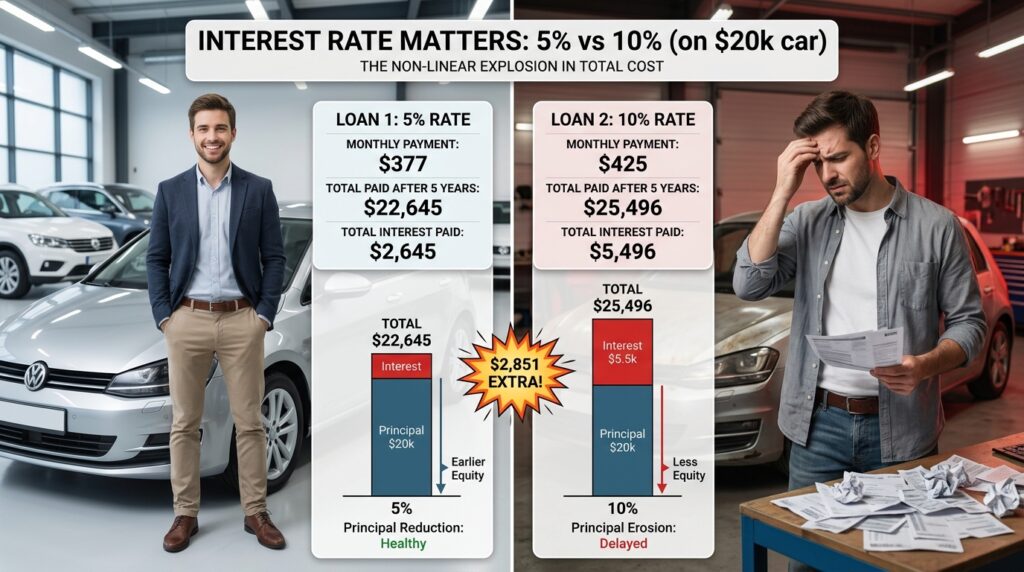

Real World Simulation: The $30,000 Comparison

Let’s look at a practical example. Imagine you’re financing a vehicle or perhaps a large home improvement project for $30,000 over a 60-month (5-year) term. We’ll compare a “Low Interest” tier (common for those with great credit or manufacturer incentives) against a “High Interest” tier (common for used cars or those with average credit).

Scenario A: The Low Interest Loan (4%)

-

Monthly Payment: ~$552

-

Total Interest Paid: ~$3,150

-

Total Cost of Loan: $33,150

Scenario B: The High Interest Loan (12%)

-

Monthly Payment: ~$667

-

Total Interest Paid: ~$10,020

-

Total Cost of Loan: $40,020

The Real Impact: Over five years, the person with the 12% loan pays nearly $7,000 more for the exact same product. Think about that for a second. That is $7,000 that could have gone into a child’s college fund, a dream vacation, or even a high-yield savings account where you earn the interest instead of the bank. The person in Scenario B is essentially paying a “penalty” of $115 every single month just for the privilege of having a higher rate.

The “Debt Trap” of High Interest Rates

One of the most dangerous aspects of high interest loans is how they limit your options if life throws you a curveball. When you have a high interest rate, you are “underwater” on your loan for a much longer period. If you need to sell the car or the asset two years into the loan, you might find that you owe $25,000 on something that is only worth $20,000.

This creates a cycle where you have to come up with cash just to get out of a debt. Low interest loans allow you to reach that “break-even” point much faster. In my experience, the biggest stressor in personal finance isn’t the debt itself; it’s the feeling of being trapped by it. High interest is the cage, and low interest is the key.

Is it worth it?

Is it ever worth taking a high interest loan? The short answer is: rarely, but sometimes it’s a necessary bridge.

If you are in a situation where you absolutely need a vehicle to get to a high-paying job, and your credit score currently dictates a 15% interest rate, you might have to take the hit. However, it’s only “worth it” if you have an exit strategy. This means taking the loan, making every payment on time for 6 to 12 months to boost your credit score, and then refinancing as soon as humanly possible to a lower rate.

On the flip side, low interest loans are almost always worth it if they allow you to keep your cash invested elsewhere. If a dealership offers you 1.9% financing while you can earn 5% in a safe treasury bond or savings account, you are actually “making” money by taking the loan. This is what wealthy individuals call “leveraging” other people’s money.

What to Consider Before You Choose

Before you sign that dotted line, you need to look at more than just the APR. Here are the critical factors:

Your Credit Health

Your credit score is the single biggest lever you have. Sometimes, waiting three months to pay down a credit card and boost your score by 40 points can save you thousands of dollars in interest. Don’t rush into a high interest loan out of impatience if a little bit of credit “hygiene” could unlock a much better tier.

The Loan Term

People often try to hide the “Real Impact” of high interest by stretching the loan out to 72 or 84 months. Sure, the monthly payment drops, but the total interest paid skyrockets. A high interest loan over a long term is a financial disaster. If you must take a higher rate, try to keep the term as short as possible to minimize the damage.

Prepayment Penalties

Always check the fine print. Some high interest lenders include penalties if you try to pay the loan off early. They know you’ll likely want to refinance or pay it off when you get your tax refund, and they want to ensure they get their “rent” money. Avoid these loans like the plague.

Important Tips

-

Shop Around: Never settle for the first rate you’re offered, especially at a dealership. Check with local credit unions; they often have much lower rates for their members than big national banks.

-

The “Total Cost” Mindset: When talking to a salesperson, stop asking “What’s the monthly payment?” Start asking “What is the total amount I will have paid after 60 months?” It changes the entire tone of the negotiation.

-

Focus on the Principal: If you are stuck in a high interest loan right now, try to pay even an extra $50 a month toward the principal. Because of how interest is calculated, those early extra payments have a massive “snowball” effect in reducing your total debt.

-

Watch Out for Fees: Sometimes a “low interest” loan comes with high “origination fees” or “document fees.” If you pay $1,000 in fees to get a 1% lower rate, you need to do the math to see if you’re actually saving money or just moving it around.

The Psychological Weight of Debt

We can talk about spreadsheets all day, but we also need to talk about how you feel when you wake up in the morning. A high interest loan feels like a shadow. It’s a constant reminder that you are working for the bank, not for yourself.

When you manage to secure a low interest loan, or better yet, pay off a high interest one, there is a literal “weight” that leaves your shoulders. Your money starts working for you. You can take risks, you can save more, and you can live with a level of peace that a high interest “debt trap” simply doesn’t allow.

Conclusion: Take Control of Your Math

The High Interest vs Low Interest Loans: Real Impact is ultimately a story of two different futures. In one future, you are the passenger, watching your money disappear into the ether of bank profits. In the other, you are the driver, using credit as a tool to build a life you love without overpaying for the privilege.

If you are currently looking at loan options, don’t be seduced by the “low monthly payment” if it’s masking a predatory interest rate. Take out your calculator, multiply that payment by the number of months, and look at the total. If that number makes you uncomfortable, it’s a sign to walk away, work on your credit, or look for a more affordable asset.

Remember, a loan is a contract with your future self. Make sure you’re being kind to that person. Choose the lowest interest possible, stay disciplined, and always keep your eye on the total cost. Your bank account—and your future self—will thank you.