We have all been there—life is moving along smoothly until a sudden unexpected event throws a wrench into our financial plans. Maybe it was a medical emergency, a period of unemployment, or simply a few mistakes made in our younger years that left our credit scores looking a bit bruised. When the time comes to buy a car, walking into a dealership can feel like a high-stakes audition. You find the vehicle you need, but the moment the finance manager pulls your credit report, the atmosphere shifts. This is the moment many drivers encounter a specific branch of the lending world: subprime auto financing. It is a path designed for those who don’t fit into the “perfect” borrower box, but it is a path that must be navigated with extreme care and strategy.

In the complex ecosystem of 2026’s automotive market, subprime auto financing acts as a bridge. It connects individuals with less-than-stellar credit—typically those with a FICO score below 620—to the vehicles they need for their daily lives. While the term “subprime” often carries a bit of a stigma due to the financial history of the early 2000s, today’s market is much more regulated and data-driven. For many, it is not just a way to get a car; it is a vital tool for rebuilding financial credibility. However, because the lender is taking a higher risk on you, the terms of these loans are vastly different from “prime” loans. To make this work for you, rather than against you, you need to understand the gears turning behind the scenes.

The Mechanics of Subprime Loans

To understand What Is Subprime Auto Financing?, you have to look at the world through the lender’s eyes. When a bank lends money to a “prime” borrower (someone with a score of 750 or higher), they are nearly certain they will get their money back. With a subprime borrower, that certainty drops. To offset this risk, lenders adjust the “levers” of the loan.

The most obvious lever is the interest rate. While a prime borrower might see rates around 4% or 5%, a subprime loan could easily range from 10% to 20% or even higher. Additionally, subprime lenders often require more documentation. They won’t just take your word for it; they’ll want to see recent pay stubs, utility bills to prove your residence, and sometimes a list of personal references. In 2026, many subprime loans are also “secured” more aggressively, meaning the lender might require a larger down payment to ensure you have “skin in the game” from day one.

The Advantage: A Second Chance at Mobility

It is easy to focus on the high costs, but subprime financing exists because there is a genuine need for it. Without these specialized lenders, millions of people would be locked out of the car market entirely, unable to get to work or care for their families.

1. Rebuilding Your Credit Score

A subprime auto loan is one of the most effective ways to “heal” a broken credit score. Because auto loans are “installment debt,” making consistent, on-time payments over 12 to 24 months shows other lenders that you have become responsible. Many of my clients have started with a subprime loan and, within two years, were able to refinance into a prime loan because their score jumped 100 points.

2. Immediate Transportation

We live in a world that doesn’t wait for your credit score to go up. If your old car dies and you need to get to your job tomorrow, a subprime loan provides the immediate solution. It allows you to maintain your livelihood while you work on your long-term financial health.

3. Professional Guidance

Subprime lenders are often more “hands-on.” They can sometimes help you choose a vehicle that is more reliable and better suited for your budget because they want to ensure you don’t default. They aren’t just selling a car; they are managing a risk, and your success is ultimately their success.

The Disadvantages: The High Price of Risk

While the “yes” feels good in the moment, the costs of subprime financing are substantial and can become a burden if you aren’t prepared.

1. Total Interest Paid

The most significant downside is the “Total Cost of Ownership.” Over a 60-month loan, a subprime interest rate can mean you pay for the car twice—once for the vehicle and once in interest to the bank. This makes the car much more expensive than it would be for a prime buyer.

2. Limited Vehicle Choice

Lenders often put restrictions on what you can buy. They might say the car cannot be older than seven years or have more than 100,000 miles. While this protects you from buying a “lemon,” it also means you might not be able to buy that older, cheaper car you had your eye on.

3. Aggressive Repossession Terms

Because the risk is high, subprime lenders are often much faster to repossess a vehicle if you miss a payment. In 2026, some vehicles are even equipped with remote “starter-interrupt” devices that prevent the car from starting if the payment is late. It is a high-pressure environment that demands 100% reliability from the borrower.

Comparing Prime vs. Subprime: The Math

Let’s look at a real-world example of a $20,000 used car.

Prime Buyer (Score 750)

-

Interest Rate: 5%

-

Monthly Payment: ~$377

-

Total Interest Paid: ~$2,620

Subprime Buyer (Score 580)

-

Interest Rate: 18%

-

Monthly Payment: ~$508

-

Total Interest Paid: ~$10,480

In this scenario, the subprime borrower pays $131 more per month and a staggering $7,860 more in total interest. This is why a subprime loan should never be a “set it and forget it” commitment. It should be a temporary stepping stone.

Is it worth it?

Is subprime auto financing worth it? The answer is a qualified “yes,” but only if you have a clear exit strategy. It is worth it if it gets you to a job that pays well, and if you use it as a tool to rebuild your credit.

However, it is not worth it if you are using it to buy a luxury vehicle you can’t truly afford. If the high monthly payment prevents you from saving money or paying other bills, you are just digging a deeper financial hole. In my opinion, subprime financing is a “medicine” for a financial illness—it helps you get better, but you don’t want to be on it forever.

What to consider before choosing

Before you sign the contract, take a breath and evaluate these three critical factors:

Your Debt-to-Income Ratio (DTI) A subprime lender will look at your gross income, but you need to look at your net income. After you pay rent, buy groceries, and pay for gas/insurance, can you comfortably afford that $500 payment? If the answer is “maybe,” the answer is actually “no.”

The Condition of the Car Since you are already paying a premium in interest, you cannot afford a car that needs $2,000 in repairs next month. Always get a pre-purchase inspection. A subprime loan on a bad car is a recipe for a financial nightmare.

The Lender’s Reputation Not all subprime lenders are created equal. In 2026, some “Buy Here Pay Here” lots disguise themselves as subprime lenders but don’t actually report your payments to credit bureaus. If your payments aren’t being reported, you aren’t building credit, which defeats one of the main purposes of the loan.

Important tips

If you have decided to move forward with subprime financing, use these tips to protect your future:

-

The “6-Month Rule”: Make every single payment on time for six months, then check your credit score. Many people see a significant jump.

-

Aim for Refinancing: Set a calendar alert for 12 months from today. By then, if you’ve been perfect with your payments, you should shop around for a refinance to a lower rate.

-

Put More Money Down: Every dollar you put down reduces the principal that is being hit with that high interest rate. It also shows the lender you are committed, which might actually lower your APR slightly.

-

Buy GAP Insurance: This is vital. Because subprime loans are high-interest, you will likely be “underwater” (owing more than the car’s value) for most of the loan. If the car is totaled, GAP insurance saves you from paying for a car you can’t drive.

-

Keep it Simple: Buy a reliable, humble car. Use the subprime loan to buy a tool, not a toy. The goal is to get from A to B while your credit score gets from 580 to 680.

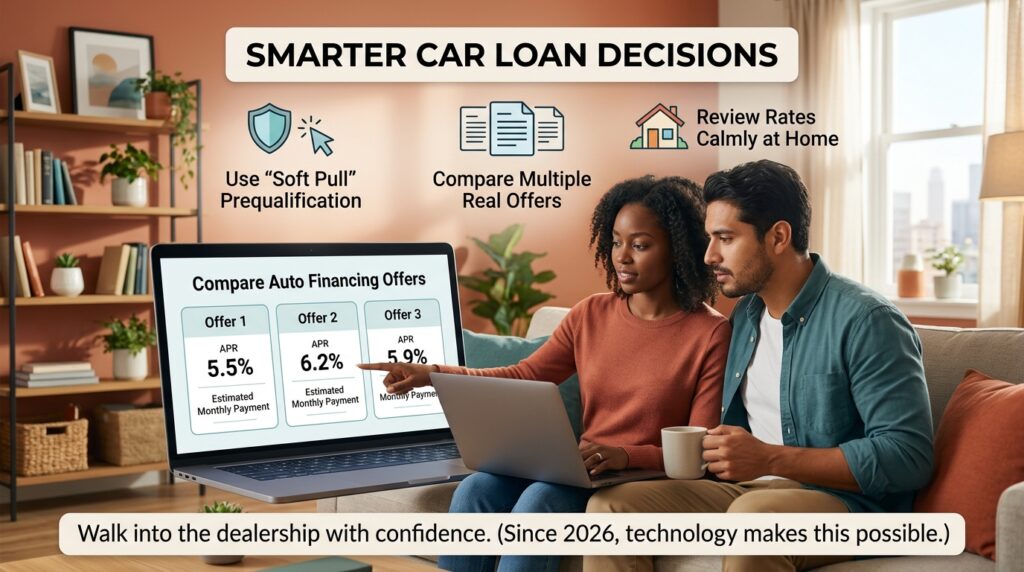

The 2026 Subprime Market: Digital Transparency

In 2026, we are seeing more “soft pull” technology. This means you can see if you qualify for subprime financing and at what rate without actually hurting your credit score with a “hard inquiry.” I always recommend using these digital tools first. Compare three or four offers from the comfort of your home before you ever step foot into a dealership’s finance office. This takes the pressure off and lets you make a logical decision.

Conclusion

Understanding What Is Subprime Auto Financing? is about recognizing it for what it is: a high-cost second chance. It is a financial tool that offers a path to mobility and credit recovery for those who have faced hardships. While the interest rates can be eye-watering, the ability to drive to work and rebuild your financial reputation is a powerful advantage.

However, the “trap” of subprime financing is staying in it for too long. If you treat a subprime loan as a permanent lifestyle, you will lose a fortune to interest. If you treat it as a 12-to-24-month bridge to a better financial future, it can be the smartest move you make this year.

Take your time, read every line of the contract, and make a plan to graduate to prime financing as soon as possible. Your car is the vehicle that moves you down the road, but your financial decisions are what move you toward your goals. Drive safe and borrow smart!